The Amazing Support Percentage of Revenues for SAP & Oracle

Executive Summary

- SAP and Oracle extract high support costs from their customers.

- SAP and Oracle also receive extremely high margins for this support.

Video Introduction: The Amazing Support Percentage of Revenues for SAP & Oracle

Text Introduction (Skip if You Watched the Video)

SAP and Oracle are very aggressive in promoting how well they are doing financially and in their technology. However, something that receives little attention is how high the support percentage of their revenues is and how much they rely upon their incomes for their profitability. Both SAP and Oracle have support margins in the 90% range. As for the revenue composition, more than 1/2 of each company’s revenues are from support. You will learn as we look back a few years to see the support percentage used to be and what this change means for how SAP and Oracle monetize their customers.

Our References for This Article

If you want to see our references for this article and other related Brightwork articles, see this link.

Notice of Lack of Financial Bias: We have no financial ties to SAP or any other entity mentioned in this article.

On Maintenance Fees

“According to Veverka (2009), Oracle’s income from maintenance fees is more than 51% of its total revenue, and SAP’s is 50% (SAP Investor Relations 2013). With all of the aforementioned issues, implementation, and associated service costs, not many can afford to go for an ERP implementation.”

This percentage has only increased since this time. The support part of the business is growing faster than the rest of SAP or Oracle’s business.

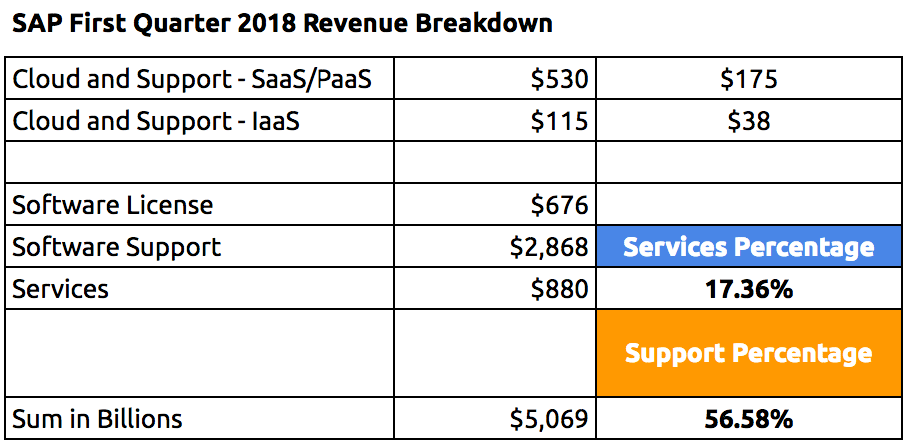

In fact, as of our calculation for the first quarter of 2018, SAP’s percentage of revenues that are made up of support is significantly higher.

The fact that the only real growth in either revenue or profitability is support for both companies should be an area of concern for those analyzing these two companies.

The Future of SAP & Oracle?

This quote brings up interesting questions for the future of SAP and Oracle.

The following quotation is from Ahmed Azmi, a person who used to work in Oracle support.

“80% of the M&S revenue comes from the top 10-20% of SAP and Oracle customers. Premier customers who spend $10 million+ on services per year. Think Fortune 500.

For this customer, a support contract is just an expensive insurance policy. Just in case something happens, the vendor must step in. They have ZERO interest in innovation value. In fact, they would never let anyone come near their stable version. That’s why most customers don’t run the latest product releases.

Any CIO worth his salt knows that new products are risky at best so they never upgrade until a few years have gone by and the most serious issues have surfaced and resolved. No one wants to be a lab rat for their software vendors.”

Ahmed goes on to explain how those that follow Oracle are being misled because of the support margins.

“Take Oracle. Sales growth over the last three years has averaged a paltry 2%. The most recent quarter showed sales growth of 3%, so it wasn’t much of an improvement. However, profit margin is 42.1%, and operating margin is 36%.

To be fair, these high margins despite stalled growth are driven by SEVERE cost cutting. Hiring fresh grads and offshoring development and support to India and Romania.

The key observation here is lack of growth catalyst. 2% growth over the past three years means the cloud numbers were fiction. This also explains the investor lawsuit for cloud fraud, and the recent departure of the head of Oracle cloud.”

Both SAP and Oracle aggressively cut costs. Both companies rely on a similar 22%+ percentage of the original license, and both follow a third-world employment model for most of their support.

Getting Profits Up With Customers Who Can’t Leave

Looked at it that way, SAP’s and Oracle’s increased margins look like a short-term strategy to get profits up (and squeeze the most squeezable part of their revenue stream). That is support…. customers who can’t leave. Wall Street does not see this and is buying the growth story pitched by McDermott and co and Hurd and co. Those analysts think those profits are coming from the non-support part of these company’s revenues. Both companies have proposed that cloud sales are what is driving this margin. However, both companies have about the same percentage of revenues that make up their cloud, around 16 percent.

What Wall Street does not see is the cost-cutting has rendered SAP and Oracle support close to inoperable. This reduces the maintainability of the solutions that were so expensive to implement. On the Q4 2018 (fiscal) call Safra Catz bragged about Oracle’s 47% margin. She did not let on to the analysts that most of that margin is in support! But the math on this is simple. Most of Oracle’s margin is from support. She and the rest of the execs on the Oracle side gave the analysts the impression the margin was generalized.

Are SAP and Oracle’s Support Margins Monopolistic?

Economists perform the study of margins to test for monopoly power. The margins that SAP and Oracle charge for support are generally referred to as “monopoly profits.”

This is an excellent example of the type of research into monopoly profits.

However, some pro-SAP resources have proposed that even though SAP’s margins are so high, SAP does not have a monopoly on SAP support because of third-party support.

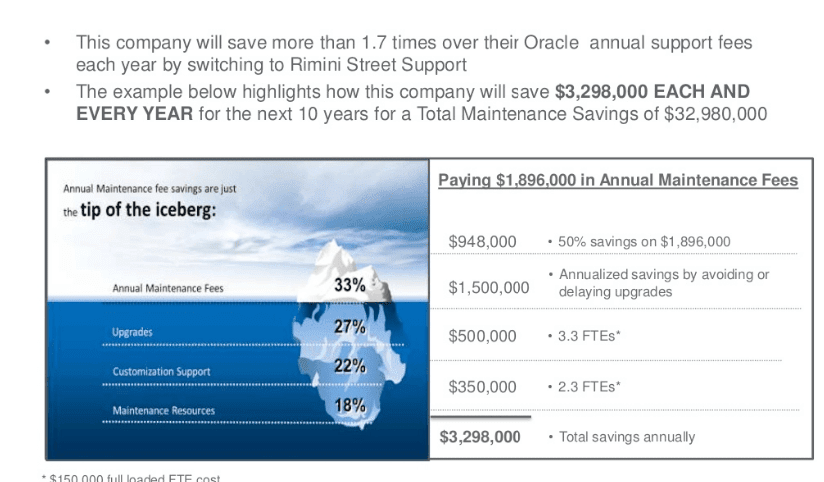

I am quite familiar with the effort that companies like Rimini Street make to get support contracts. First, Oracle’s margins are so high that Rimini Street promises a 50% cost reduction right off the bat.

Rimini Street has popularized these types of graphics, explaining the annual support fees are only one part of the costs associated with keeping Oracle and SAP operational. Both SAP and Oracle always push upgrades that consume more resources and have little impact on improving the software. Rimini Street has explained upgrades cost, and the price is very high. Many upgrade projects become costly affairs with a lot of billed hours for consulting firms.

Some problems make SAP and Oracle’s support sticky. First, an SAP and Oracle’s customer getting off of support means they don’t get upgrades. If this tie were broken many, more companies would far more readily switch away from SAP and Oracle’s support.

Moreover, once we get beyond Rimini Street, who is there? Well, there is Spinnaker Support, but Spinnaker is very small in SAP support. SAP customers don’t have many options. Oracle has more options, but it is still very little competition. Secondly, if you are going to provide 3rd party support (and be public about it), you better have a lot of money set aside for attorneys. Oracle has repeatedly been suing Rimini Street in an attempt to put them out of business.

Conclusion

SAP and Oracle’s support revenues and profits are called monopolistic profits by economists, a topic we cover in more detail in the article How do SAP and Oracle’s Support Margins Compare to Pablo Escobar. They are so high because it is constrained. This allows SAP and Oracle to offer extremely little value in return for the support dollars.

SAP and Oracle’s support revenues and profits are the primary drivers within these companies. This means that their strategies will increasingly reflect their motivations to protect these revenues and margins. Secondly, both companies are using these revenues and profits to project health in the rest of their businesses to Wall Street. At some point, these companies will not be able to maintain this illusion.