How to Most Effectively Manage the Foreclosure Process

Executive Summary

- People facing foreclosure are often overwhelmed with the information they are provided.

- This article will help clarify one’s options and what to do next.

Introduction

- This article will include some of the best quotations that we could find about dealing with foreclosure.

- Secondly, we provide both the backdrop for foreclosure as it is interpreted by banks, then cover the options for people who are in foreclosure.

- At the end of the article, we discuss how to get help and support for people going through a foreclosure.

Setting Your Mentality for Managing the Foreclosure Process

Foreclosure is a difficult psychological prospect for mortgage holders. It places stress on the mortgage holder, which makes it less likely that they will fully evaluate the options that are available to them. There is also a general misunderstanding that once the final date of payment prior to foreclosure has passed that all of the mortgage holder’s options are gone.

This is not the case.

That is one of the most important things for the mortgage holder to understand. In many cases, it is a lack of understanding that got the mortgage holder into the foreclosure situation. There are cases where medical or job loss leads to foreclosure. Still, in one way or another, the mortgage holder did not consider the implications of the decisions that they made earlier in the process, often being too optimistic. The mortgage holder must not take that same type of misunderstanding or a passive approach into the foreclosure process.

Experience with Foreclosure?

Another major problem is that most people who go through foreclosure have never been through the foreclosure process.

- The first thing to remember is to stay calm and be rested so that you can interpret information and follow through on the options.

- The second thing to remember is that the foreclosure process provides a number of options that can either the mortgage holder regaining the house or pulling important equity out of the house.

Coronavirus

This article was written in 2018. However, it has been updated as it more relevant than ever as we are about to head into possibly record foreclosures during the Coronavirus of 2020.

The vast majority of financial assistance has gone to the largest financial entities in the US economy.

Question #1: What Are the Bank’s Incentives During a Foreclosure?

It is very easy to conclude that the bank wants its mortgage lenders to go into foreclosure so that the bank can sell the house for a profit. However, foreclosure is not what the bank desires. And the primary reason for this turns out to be that the bank is really set up to collect payments rather than selling and managing foreclosed houses.

This is covered in the following quotations:

“What is the secret that the bank does not want you to know? The bank does not want to take away your home! I know it sounds absurd, but by the time you finish reading this article you will be persuaded that it is an accurate statement. Allow me to go a step further; the very last thing that the bank wants to do is foreclose on your property. It will become an extra expense that they don’t need to incur and it will cost them thousands of dollars to take a property through the foreclosure process. Now you may be asking yourself: If that’s true, why are they threatening me with foreclosing my property? What do they really want?

There is a simple answer: the bank collection agent wants to scare you into making up the late mortgage payments, and by doing so, ensure you will continue to make your payments on a regular basis until the end of the term as specified in the mortgage agreement. The threat of foreclosure is the only tool that the bank has at its disposal to persuade you to make the mortgage payments.” – Huffington Post

This brings up the question of the internal incentives of the bank. The bank is set up to give out loans and process payments, and foreclosures put a wrench into that process.

What Happens When a Loan is Declared a Non-Performing Asset?

As the next quotation will illustrate, it negatively impacts the bank once the status of the loan is changed from performing to non-performing.

“Once the bank initiates the foreclosure process, the laws regulating the banking industry require them to report that property as a non-performing asset. Doing this will hinder the bank’s capacity to borrow more money and will affect its overall credit rating.(emphasis added) The bank must try to avoid having to report a non-performing asset on its books at all cost.(emphasis added) In many cases, banks intentionally delay initiating a foreclosure proceeding for up to six months, and sometimes even up to a full year, to avoid reporting the property as a non-performing asset.

The ‘non-performing asset’ problem or the NPA, as it is commonly known in the banking and financial industry, affects the banks in more ways than you and I may care to know. These three simple letters strike terror in the banking sector and business circles. The dreaded NPA rule simply states that: “When interest on a loan or any other monies is due to a bank and it remains unpaid for more than 90 days, the entire bank loan automatically becomes a non-performing asset.” They will go to great lengths to avoid having to report a property as a non-performing asset.(emphasis added)

There are a number of problems that will arise from having too many NPAs on the bank’s books. The biggest problem is that the bank must have a certain amount of dollars in cash reserves. If their levels of non-performing assets become too high, they will have to put more cash into their reserve account to compensate for these non-performing assets. This means they now have less money to lend. In addition, they now have to deal with a house that they don’t want because it will become a money pit. Furthermore, they will not be able to make a profit on it because of the way mortgages are structured.” – Huffington Post

Question #2: Do Banks Make Money on Foreclosures?

It is natural to assume that banks make money on foreclosures. Yet surprisingly, in most cases, they don’t.

This is covered in the following quote.

“In a foreclosure case, they will most likely lose money. Having the knowledge of how lending institutions operate is empowering. Since you now know that lenders don’t want to foreclose on your property — and you don’t want them to foreclose on you — you have common ground to work out an agreement that will stop the foreclosure process and satisfy both of your needs. Remember: The bank does not want to foreclose your property.” – Huffington Post

The next quote gets to the core of the bank’s incentives.

“Up until the time your home is scheduled for auction, most lenders would rather work out a compromise that would allow you to get back on track with your mortgage than take your home in a foreclosure.” – HGTV

This is a critical observation about how foreclosures work for banks. While it may seem that the bank has all the leverage; in fact, the mortgage holder still has leverage because what the bank is threatening to do, it does not actually want to do.

Question #3: How Did the Bank React to Foreclosures During the Housing Crises of 2009+?

Because of these incentives, there have been a number of cases where banks forestalled foreclosures in mass during a period when they had to deal with many foreclosures.

“We’re seeing more and more, banks getting a judgment to sell a home but not taking it to a foreclosure sale,” says Thomas Fitzpatrick, an economist in the community development department at the Federal Reserve Bank of Cleveland. “Banks speak more openly about how if it’s not in their economic interest to foreclose, they’re not going to foreclose. It may cost more to cure the back taxes and bring the property up to code than they could ever get from selling the property itself.”

“We call them zombie foreclosures,” says Daren Blomquist, vice president at RealtyTrac, which estimated with the number of abandoned foreclosures by cross-referencing addresses of homes in the foreclosure process in the first quarter with vacant property data from the U.S. Postal Service.

“If it’s going to cost us $30,000 to foreclose and the unpaid balance on the loan is $30,000 and current market value is not much higher, we might release the lien and give the home back to the borrower.” – American Banker

For the bank, foreclosure is a straightforward affair, but for mortgage holders, it will often overwhelm them. This leads to problems in dealing with the foreclosure process.

Question #4: What Are The Credit Implications of a Completed Foreclosure?

Another reason to not sit back passively as a foreclosure occurs is the effect on the mortgage holder’s credit. The more active the mortgage holders are, the better the outcome as the mortgage holder can, even in situations where the house is lost, manage the impact on their credit. In situations where the house cannot be kept, the goal would be to stop the final foreclosure event from ever occurring (the options for which we will cover further on in this article.)

“Foreclosure, be it voluntary or involuntary, can be very damaging to your credit. Your mortgage records will be marked as in foreclosure, and these records will remain on your credit files for seven years. A mortgage foreclosure is nearly as damaging as a bankruptcy filing and will have a significant impact on your ability to borrow in the future.” – HGTV

The Timing of the Foreclosure Process

Let us review the timing of the foreclosure process.

“The first thing that will occur in the foreclosure process is that the lender will record a Notice of Default. From here, you have 90 days to pay what you owe. After 90 days, if you have not made your payments, a Notice of Sale will be recorded and sent to you by certified mail. The notice will also be published in a newspaper and posted on your home and in a public place, such as the local courthouse. After a minimum of 21 days from the Notice of Sale being recorded, the house will be put up for auction; you will immediately lose control of your home once it’s sold.” – Global Banking Rates

“In many cases, the foreclosure process will start three to six months after they’ve missed their first payment.” – HGTV

Foreclosure has a number of options that are available to mortgage holders. Some are better than others, and the option to be employed sometimes depends upon what stage of the process the mortgage holder is in.

The earlier the mortgage holder is in the process, and the more they can access a source of funds, the better the outcome for the mortgage holder.

Question #5: What Are The Options in the Foreclosure Process in the US?

There are five options we could find that are active options for dealing with the foreclosure process.

The options available in the foreclosure process are the following:

- Pay Off the Loan and Foreclosure Expenses

- Pay Off Loan Payments and Associated Costs

- Request the Bank to Produce the Note

- Deed in Lieu of Foreclosure

- Short Sales

- Declaring Bankruptcy

Let us go through each of the options.

Option #1: Pay Off the Loan and Foreclosure Expenses

This is an option, but not one that is available to many people, as if the mortgage holder could do this, they would not be in foreclosure in the first place.

This is explained in the following quotation.

“A property owner can stop a foreclosure process if he or she pays off the loan and all of the lender’s foreclosure expenses and costs.” – HGTV

Option #2: Pay Off Loan Payments and Associated Costs

This is actually the best option. This means the mortgage holder must find the funds to do so. But it stops the foreclosure process.

This is explained in the following quotation.

“Pay the mortgage holder any loan payments you are behind on together with any interest, fees or late charges incurred by the mortgage holder. Although this is the most difficult thing to do since you are already in default because you haven’t made timely payments, this is the best way to prevent foreclosure proceedings.” – HGTV

It will mean negotiating with the bank, but remember, the bank does not want to foreclose if they can find a reason not to.

Option #3: Deed in Lieu of Foreclosure

A deed in lieu of foreclosure is something for the last stage of the foreclosure. Therefore it is something after all the options have been exhausted.

This is explained in the following quotation.

“Some states permit strict foreclosures or deeds in lieu of foreclosures. In those states, when a property owner defaults on the terms of the mortgage, the court orders the property owner to pay the mortgage within a certain period of time. If the property owner can’t satisfy the court order within that time frame, the lender, or mortgage holder, is permitted to take the title of the property.” – HGTV

“At the auction, the home is sold to the highest bidder. The big catch is that these auctions require cash payment in most states; few third-party buyers can afford to bring enough cash to the courthouse to pay in full. As a result, many lenders either simply ink an agreement with the homeowner to take the property back (called a deed-in-lieu of foreclosure — see No. 4 in 5 Ways You Can Stop the Foreclosure Process) or buy it back themselves at the auction.” – HGTV

Option #4: Short Sales

A short sale is where the mortgage holder cannot or will not pay the mortgage, but sells the house instead of the bank selling the house.

This is explained in the following quotation.

“A pre-foreclosure home that goes up for sale is referred to as a short sale. (Note, however, that not all short sales are pre-foreclosures). Because the property owner wants to avoid foreclosure, an interested party may be willing to purchase the pre-foreclosed property for a higher value than the seller would get if the home was sold in a foreclosed state. The sale can be a private transaction between the homeowner/seller and the buyer whose offer must be approved by the bank before the sale can be finalized. A pre-foreclosed home can be inspected by the buyer before the buyer makes an offer on the home. The buyer could be an investor who prefers to purchase the home for much less than it’s worth, renovate and repair the home if needed, and then sell it at a higher price for a profit.

A home that is sold during the pre-foreclosure phase may be a win-win-win for all three major parties involved. The homeowner is able to sell his property which he can no longer afford to keep while avoiding the damage that a foreclosure would have on his credit history. The buyer may be able to snag the property for below market value price after inspecting the property. The lending institution that approves the buyer’s offer is able to transfer the mortgage to the buyer, and avoid the cost of going through a foreclosure”. – Investopedia

“After your lender files an NOD but before they schedule an auction, if you get an offer from a buyer (that is a short sale), you lender must consider it. If they foreclose on your home, the lender is going to simply turn around and try to resell it; if you present them with a reasonable short sale offer, they may see it as saving them the time, effort and trouble of finding a qualified buyer in a soft market. So, if your home is on the market, continue to aggressively seek a buyer for it, even after your lender initiates the foreclosure process. Read our guide on How to Sell Your Home Fast When Foreclosure Looms for action steps you can take to unload your home fast, then make your best pitch as to why your lender should agree to the short sale.” – HGTV

Option#5: Declaring Bankruptcy

This is an extreme technique that does more to forestall the foreclosure than to fix the situation, and of course, it adds the negative feature of bankruptcy to the mortgage holder’s credit.

This is explained in the following quotation.

“Bankruptcy stops foreclosure dead in its tracks. Once you file a bankruptcy petition, federal law prohibits any debt collectors, including your mortgage lender, from continuing collection activities. Foreclosure is considered a collection activity, and so the day your lender becomes aware that you have filed for bankruptcy, the foreclosure process will effectively be frozen. But here’s the rub; once you get to court, the bankruptcy trustee’s role is simply to play referee or mediator between you and your creditors. Bankruptcy really just buys you more time to replace your lost job or recover financially from a temporary disability; it doesn’t let you off the hook for your debts. The law requires your mortgage company and other creditors to work in good faith with you to formulate a reasonable repayment plan so you can get back on track. Consult with a bankruptcy attorney regarding whether filing for bankruptcy is a good strategy for you.” – HGTV

Option #6: Request the Bank to Produce the Note

In a study of 1700 foreclosures, 40% of the lending institutions could not find the original loan documentation. This is more of a stalling tactic, but sometimes stalling is what the mortgage holder needs to marshal funds to stop the foreclosure process.

Something to Remember When Negotiating with the Bank

“Never make a verbal agreement; always get it in writing.” – HGTV

Option #7: Getting Help from HUD

The US Department of Housing and Human Services or HUD offers counseling and even financial assistance for mortgage holders faced with foreclosure.

HUD has options and services for people in the foreclosure process.

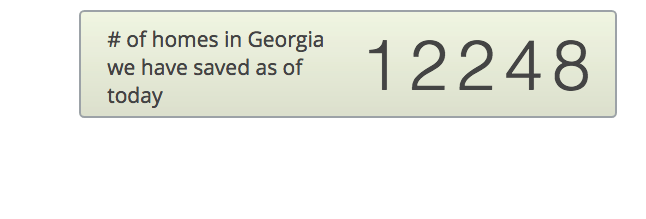

The following is from the HomeSafe Georgia website. Notice the number of homes they state they have saved.

The following is a quotation from the website.

“Use “Keep Your Home *Insert State of Residence.com”

HomeSafe Georgia is a limited funded program and not all eligible homeowners may receive assistance before funds are exhausted. Application to HomeSafe Georgia does not guarantee funds will be available or assistance will be provided.

Mortgage Reinstatement Assistance

The Mortgage Reinstatement Assistance program helps homeowners catch up delinquent

mortgage payments caused by a qualifying financial hardship. For eligible homeowners, the program provides a one time payment of up to $50,000 submitted directly to the

lender/servicer to bring the loan current.Mortgage Reinstatement Eligibility Requirements

The term “Applicant” includes all homeowners and borrowers legally responsible for the home, plus the spouse of the residing homeowner, even if the spouse is not a borrower or homeowner. The program applies only to an applicant’s primary residence. The total mortgage lien balance on all mortgages for the property does not exceed

$453,100.

The mortgage is two or more months delinquent.

The amount needed for reinstatement does not exceed $50,000.

The current gross household income supports the mortgage payment.

The mortgage delinquency was caused by a qualifying type of hardship, such as:

Phone 770-806-2100, or toll free 1-877-519-4443

Para asistencia en Español, presiene (4) cuatro

TDD/TYY Line 404-679-4915, or toll free 1-877-204-1194

Email: homesafe@dca.ga.gov”

Using a Foreclosure Attorney

“Find a lawyer to represent you when negotiating with lenders — it will ensure the best possible outcome.” – HGTV

The following is an example of the website of a foreclosure attorney in Atlanta.

The bank will respond differently if they believe they are dealing with just the mortgage holder versus dealing with both an attorney and someone experienced in the foreclosure process. Normally it makes sense to explore after exploring the support from HUD. But it does make sense to engage in a free consultation with them to determine what they can provide.

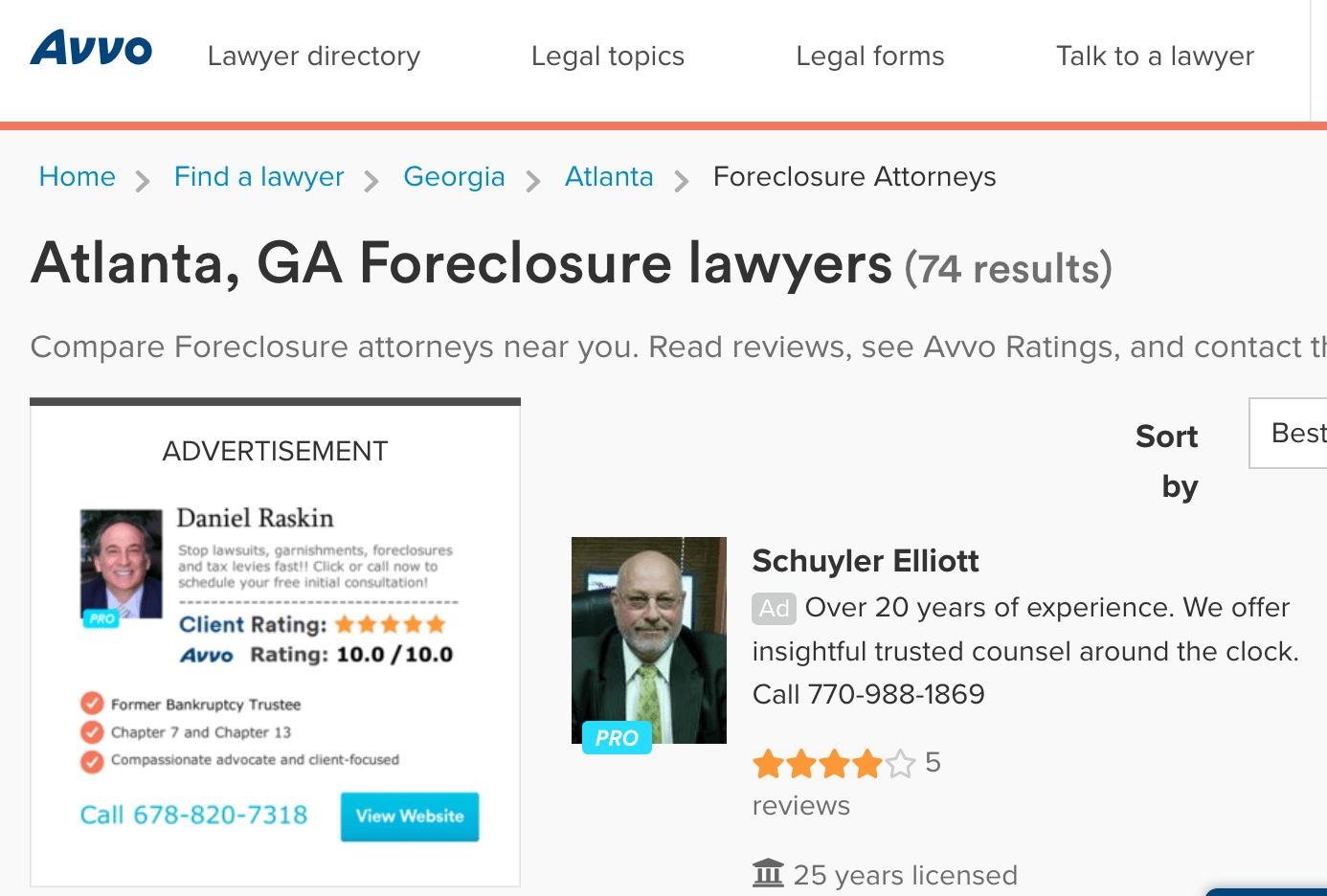

Avvo is a website that allows for searching for attorneys, and it can be filtered specifically for foreclosure attorneys.

Conclusion

There are a lot of options available to mortgage holders open to looking at their options.

- Mortgage holders in the foreclosure process should determine which option is best for them, along with exploring counseling options available through HUD.

- There is help and specialized knowledge that the mortgage holder will not have (as they don’t deal with foreclosures for as a profession) through HUD counselors and through foreclosure attorneys.

References

*https://www.credit.com/debt/understanding-your-foreclosure-rights/

https://www.hgtv.com/design/real-estate/the-stages-and-phases-of-the-foreclosure-process

https://www.rocketlawyer.com/article/foreclosure-law-what-banks-can-and-cant-do-cb.rl

https://www.huffingtonpost.ca/joaquin-benitez/home-foreclosure-canada_b_3563178.html

https://www.americanbanker.com/news/banks-halting-foreclosures-to-avoid-upkeep

https://www.gobankingrates.com/loans/mortgage/how-many-payments-can-miss-before-foreclosure/

https://www.investopedia.com/terms/p/pre-foreclosure.asp

*https://www.thetruthaboutmortgage.com/foreclosure-help/

https://www.hud.gov/offices/hsg/sfh/hcc/hcs.cfm

https://apps.hud.gov/offices/hsg/sfh/hcc/hcs.cfm?webListAction=search&searchstate=GA#searchArea

https://www.homesafegeorgia.com/

https://www.atlantaattorneysatlaw.com/

https://www.avvo.com/foreclosure-lawyer/ga/atlanta.html

https://www.consumerfinance.gov/fair-lending/