Is High Private Debt Negatively Related to Economic Performance?

Executive Summary

- There are many statements made about the appropriate debt level of countries.

- What is often lacking is comparative evidence of how private debt and public debt contribute to or undermine economic performance.

Introduction

There is great debate as to what is the correct level of private debt. This article will look at different sources on this topic.

Our References for This Article

If you want to see our references for this article and other related Non Status Quo articles, see this link.

Question on Debt

While is common to talk about public debt is too high, there is normally very discussion about when private debt levels become too high and its impact on the economy, stock market, and economic growth.

The Case of Japan’s Debt

It is often proposed that Japan’s high government debt has interfered with its economic growth since the mid-1990s.

This often leads to the conclusion that Japan’s debt level is related to its poor performance since the 1990s. However, I could propose the opposite. It was Japan’s decline that led to their increased debt. And one way of observing this is the decline in private debt. And this will be shown in a graphic very shortly.

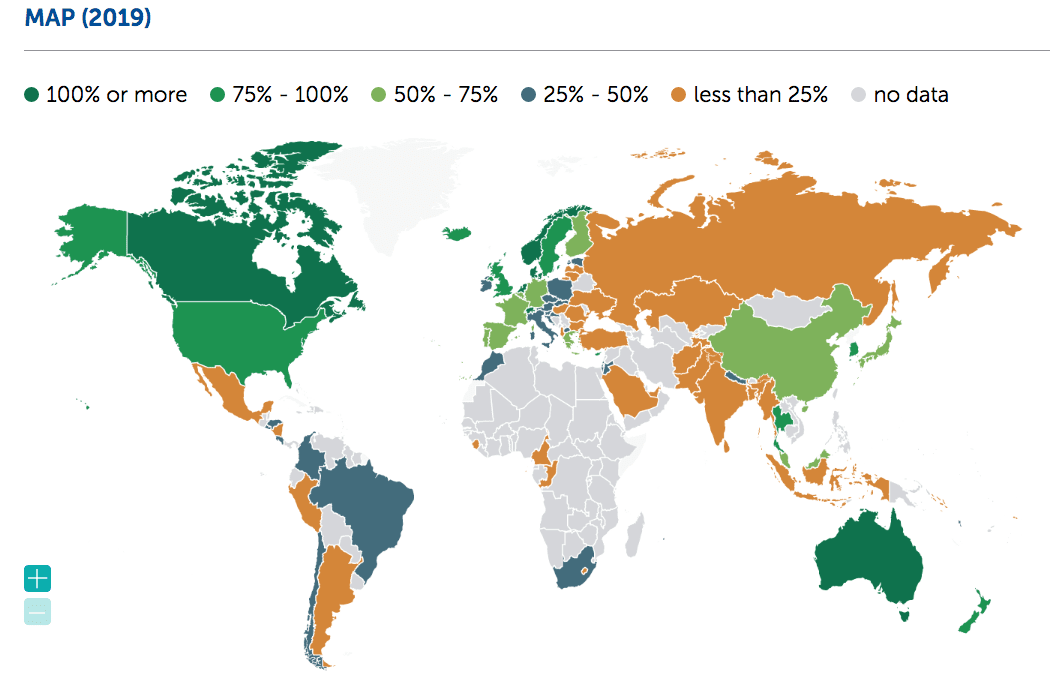

The Private Debt to GDP Ratio Per Country

Another major topic of discussion is the private debt to GDP ratio. Public debt is held by governments, private debt is held by people and companies. The public debt percentage of GDP differs greatly by country. The following is this percentage by country.

It is clear from reviewing the graphic above that the low total debt (private) is not a feature of successful economies. In fact, it is the exact opposite. Notice that the more well-off countries have a HIGHER private debt to GDP ratio, not lower. (graphic from the IMF)

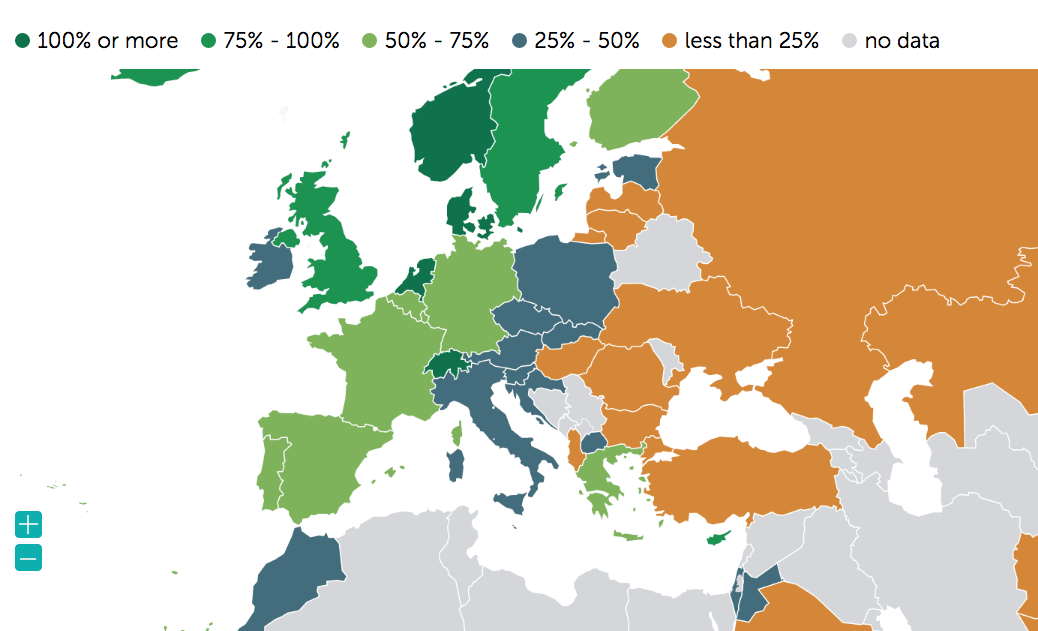

Notice the strong distinction between Western Europe, Central Europe, and Eastern Europe. It is small, but if you focus on it, you can see it clearly. Let us zoom in.

This is the zoomed-in view. The debt to GDP ratio is positively correlated with the level of the economy.

Interestingly, the least developed countries don’t have any data on the debt to GDP ratio. And this is from the IMF.

Why is there so little data for these countries? Africa has almost no data on this metric. However, overall their private debt to GDP is low. But that is clearly not a good thing.

Richard Vague on Private Debt and the Economy

Economist Richard Vague states that the real issue that foretells problems in an economy of a country is when private debt becomes too high, not public debt as is proposed by mainstream economists.

This is curious because if you look at the statements of Republican politicians, they are normally perfectly fine with high levels of debt and predatory loans and very high-interest rates on loans, even when the cost of capital is meager. This is, of course, what their campaign contributors want. However, what they don’t like, and the only type of debt they talk about is public debt — but only when Democrats control spending. When Republicans are in control of spending, the debt is barely mentioned. The way Republicans talk about debt can be synthesized down to this table.

The relationship between private debt and the economy is explained in the following quotation from Richard Vague.

What’s astonishing is how little attention the global debt problem—the extremely high ratio of private debt to GDP—has gotten. Not only does it leave the U.S. and other countries vulnerable to crisis should brisk growth in that ratio resume, but, quite apart from any crisis, the accumulation of higher levels of private debt over decades impedes economic growth. Money that would otherwise be spent on things such as business investment, cars, homes, and vacations is increasingly diverted to making payments on the growing debt— especially among middle- and lower-income groups that compose most of our population and whose spending is necessary to drive economic growth. Debt, once accumulated, constrains demand.

The ideal condition for growth is to have less capacity (that is, the supply of housing, factories, etc.) than demand, coupled with low private debt. This was the case during the decades immediately after World War II. But now we have nearly the opposite situation. In the first decade of the 2000s, the United States and Europe built far too much capacity, especially in housing, and incurred too much private debt. In the 1980s, Japan built far too much capacity, saddling its banks with too much private debt and too many bad loans. While all these countries have been catching up to this capacity, none yet has less capacity than demand, and all still have high private debt. And now China, whose industrialization and urbanization long fueled global growth, has created its own overcapacity and private debt problem, building far too much capacity in the form of industrial and real estate projects while providing easy credit that fueled a rapid buildup of private debt. So no major global economic player now has that pivotal combination of undercapacity and low private debt that can fuel productive investment and help boost global growth.

What’s more, excessive private debt may contribute to one of the great problems of our time: growing income inequality and the hollowing out of the middle class. The middle class tends to grow when there is too little capacity and low private debt (as after World War II). In contrast, the middle class plateaus or shrinks when there is too much capacity and too much debt (as at the present). Stated differently, inequality increases when there is high capacity and high debt; it decreases when capacity and debt are low. – Richard Vague

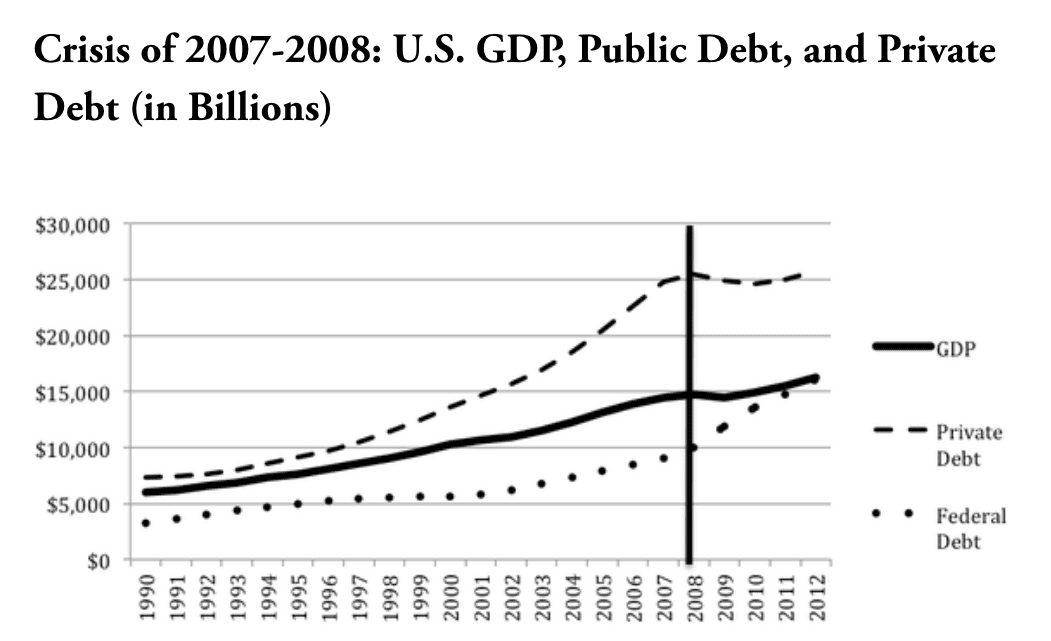

Vague points to this graph to illustrate that private debt’s growth preceded the 2007 and 2008 Great Recession.

This is Vague’s commentary on this graphic.

What was the big problem? Look at the line representing private debt. It clearly is not parallel to the GDP line and, indeed, reflects a rapid growth of private debt relative to GDP. By itself this isn’t shocking. We all know that a growth in home mortgages preceded the crash, and home mortgages are one kind of private debt—along with other consumer borrowing and borrowing by businesses. What’s more surprising is what we found when we looked at lots of other financial crises around the world, dating back to the 19th century: Though most of these crises aren’t thought of as being fundamentally caused by excessive private debt, the fact is that they were preceded by the same kind of runup in private debt that the U.S. saw prior to 2008.

Vague’s assertions checks out with other historical financial bubbles. In 1929, the US debt to GDP ratio was 16%. However, in response to the Great Depression, within a few years, the ratio had increased to 40% by 1934. Was 16% the correct level, which was when the US economy had a large amount of fraud but looked good, or was the 40% level the right level of debt when the US was in the depth of the Great Depression? From 1962 to 1988, the US public debt was less than 50% of GDP. These are generally considered very good years for the US economy — although the wages began to flatline after 1972 as unions began to lose their power.

Vague continues.

What’s alarming is that, of the two ingredients for an economic crisis—high private debt and rapid private-debt growth—one is still with us even after the 2008 collapse. Private debt in the U.S., relative to GDP, stands at 156 percent. That’s lower than the 173 percent it reached in 2008, but it’s still nearly triple the level—55 percent—it was at in 1950. Indeed, across the globe there has been a steep climb in the ratio of private debt to GDP over that period.

*This article by Vague was written in 2014. It has gone up significantly since this time.

My math shows a private debt to GDP ratio of 2.5. However, I am not sure that my calculation is the exact same as that used by Vague. For some reason, the total public debt is not easily findable so I had to calculate it.

However, you can see the method. I took the total debt and subtracted all of the public sources or categories of debt. I also found another source that calculated roughly the same value as me (lower, but for previous years as their years stopped in 2018). This may mean that Vague is using a different calculation for determining the ratio.

However, Vague was concerned in 2014 about the private debt ratio to GDP and this ratio has only grown from that time.

Vague continues..

One form of deleveraging is to provide relief for borrowers. This spurs economic growth, because by and large borrowers—especially middle-income and lower-income consumers—are likely to use the extra money to make purchases that stimulate the economy.

So what we need to do is remove some of the debt burden weighing down middle-income and low-income people. You can call it debt “restructuring” or you can call it (partial) debt forgiveness. Either way, it’s needed.

This is exactly the assertion made by banking specialist Michael Hudson.

Hudson explains that debt forgiveness was common in ancient times. In Sumeria, the debts were wiped out upon the death of a king. This was referred to as jubilee year.

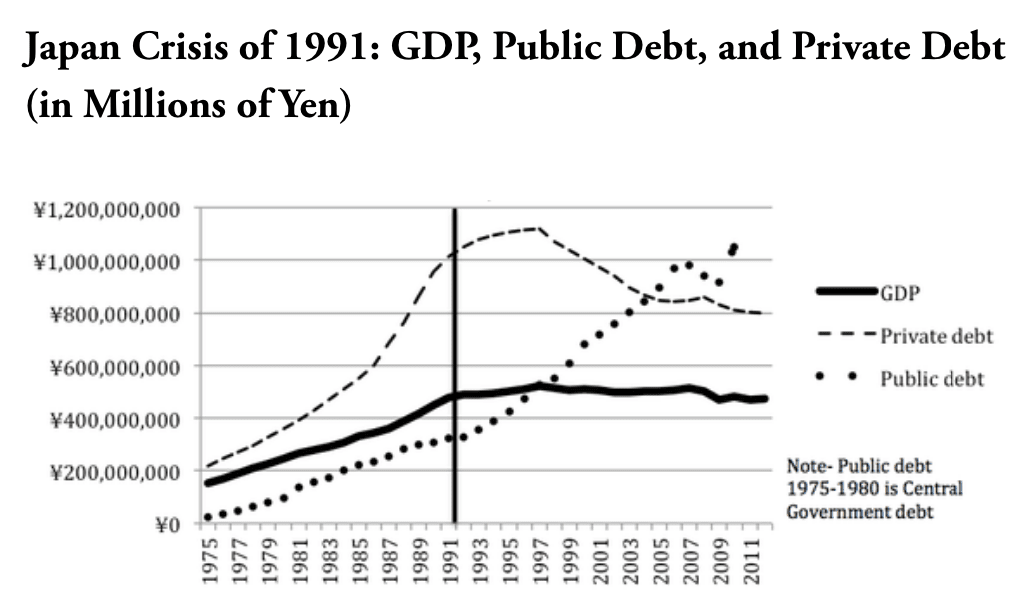

And now we will turn to the topic of Japan.

Vague points to the same pattern in Japan who’s bubble broke in the mid-1990s. The private debt in Japan begins to rise around 1985 steeply. It rises dramatically until roughly 1993. Since around 1997, private debt in Japan has gone down, while public debt has increased and even surpassed private debt around 2003. This illustrates that Japan was in a huge speculative bubble from 1985 to around 1997. Recall that expectations were sky high at this time for Japan’s future. Not only did most of the world not predict the rise of South Korea and Japan losing some manufacturing to competing countries, but very few people predicted that Japan would not be able to translate its success in precision manufacturing to other industries.

You can see that that the private debt line tracks relatively closely with the GDP line. The same thing is true for the previous US graph. The private debt and GDP lines are much more highly correlated than the public debt line.

The situation in Japan is explained by the following video from Steve Keen.

Conclusion

Very low private debt levels or very high debt levels are not desirable. When private debt levels are very low, it means that the economy is either functioning at a low level — such as the case with Latin America and Africa. However, when private debt levels are very high — for what a country historically has experienced, this means that the economy is in a bubble. According to Steve Keen, a reasonable level of private debt to GDP is between .6 to 08. During the bubble, the relationship between the asset bubble and private debt growth is explained by Ray Dalio as follows.

The key reason for the long term debt cycle can be sustained for so long is that central banks progressively lower interest rates, which raises asset prices and in turn people’s wealth, because of the present value effect that lowering interest rates has on asset prices. This keeps debt service burden from rising and it lowers a monthly payment cost of items bought on credit. But this can’t go on forever. Eventually the debt service payments become equal to or larger than the amount debtors can borrow and the debts. That is the promise to deliver money become too large in relation to the amount of money in existence there is to give when promises to deliver money, ie debt can’t rise anymore relative to the money and credit coming in the process works in reverse and de leveraging begins. Since borrowing is simply a way of pulling spending forward the person spending $60,000 per year and earning 50,000 per year, has to cut their his spending to 40,000 for as many years as he spent 60,000 All other things being equal, this is a bit of an oversimplification, but this is the essential dynamic that drives the inflating and deflating of a bubble. Bubbles usually start as over extrapolations of justified bull markets the bull market is initially justified because lower interest rates make investment assets such as stocks and real estate more attractive as they go up, and economic conditions improve which leads to economic growth and corporate profits, improve balance sheets and the ability to take on more debt, all of which make the company’s worth more, as assets go up in value networks and spending income levels rise. The boom also encourages new buyers who don’t want to miss out on the action to enter the market fueling the emergence of a bubble, quite often on economical lending and the bubble occur because of implicit or explicit government guarantees that encourage lending institutions to lend recklessly. As new speculators and lenders enter the market, and confidence increases credit default credit standards fall. Banks lever up and new types of lending instruments that are largely unregulated to develop. The lenders and the speculators make a lot of fast easy money which reinforces the bubble by increasing the speculators equity, giving them the collateral they need to secure new loans at the time. Most people don’t think that is a problem because, to the contrary, they think that what is happening is a reflection and confirmation of the boom. This phase of the cycle typically feeds on itself taking stocks. As an example, rising stock prices lead to more spending an investment which raises earnings which raise the stock prices which lowers credit spreads and encourages increased lending, which affects spending and investment rates, etc. During such times, most people think the assets are a fabulous treasure to own and consider anyone who doesn’t own them to be missing out. Humans by, by nature, tend to move in crowds and weigh recent experience more heavily than is appropriate in these ways and because of consensus view is reflected in the price extrapolation tends to occur. At such times increases in debt to income ratios are very rapid the above chart shows the archetypal path of debt as a percentage of GDP for the deflationary de leveraging as we averaged. The typical bubble she’s leveraging up to an average of 20 to 25% of GDP. Over three years or so, the blue line. This is the change in GDP. This is a change in debt to GDP ratio.

The Monetary Policy

In many cases monetary policy helps inflate the bubble rather than constrain it. This is especially true when inflation and growth are both good and investment returns are great such periods are typically interpreted to be a productivity boom that reinforces investor optimism as they leverage up to buy investment assets in such cases, central bankers focus on inflation and growth are often reluctant to adequately tighten money, that is what happened in Japan in the late 1980s, and in much of the world in the late 1920s In the mid 2000s.

In my opinion, it’s very important for central banks to target debt growth, with an eye towards keeping it at a sustainable level. That is a level where the growth in income is likely to be large enough to service a debt, regardless of what credit is used to by shadow bankers sometimes say that it is too hard to spot bubbles and that it’s not their role to assess and control them, that it’s their job to control inflation and growth but what they control is money and credit and when that money in credit goes into debt that can’t be paid back, that has huge implications for growth and inflation down the road, the greatest depressions occur when bubbles burst and if the central banks that are producing the debts that are inflating them won’t control them. Then who will the economic pain of allowing a large bubble to inflate and then burst is so high that it is imprudent for policymakers to ignore them, And I hope that perspective will change.

Thinking about the whole economy central banks typically fall behind the curve during such periods and borrowers are not yet, especially squeezed by either a higher debt service costs, quite often at this stage their interest payments are increasingly being covered by borrowing more rather than by income growth a clear sign that the trend is unsustainable. All this reverses and the bubble pops and the same linkages that inflated the bubble make the downturn self reinforcing falling asset prices decrease both the equity and collateral values of leveraged speculators which causes lenders to pull back this forces speculators to sell driving down prices even more.