Quotes from the Book The New Great Depression

Executive Summary

- The excellent book The New Great Depression was interesting, it was necessary to record some quotes.

Introduction

This book covers a scenario that is the opposite of the often projected recovery that would come as the pandemic recedes from its current heights.

Our References for This Article

If you want to see our references for this article and other related Non Status Quo articles, see this link.

What Happened in Previous US Recessions or Depressions?

In fact, stocks did not regain their 1929 highs until 1954, a full twenty five years later. Unemployment declined from its peak of 24.9 percent in 1933 yet remained about 14 percent until 1941. A similar pattern prevailed from 1873 to 1897, a period economic historians call the Long Depression.

The Evidence on Ventilators for Treating Covid

The evidence is now stonrg that overuse of ventilators did more harm than good in COVID-19 cases and cased death in many cases. Most patients don’t need a mechanical lung. They need oxygen.

It also leaves open the possibility that second wave of infections may arrive in 2021 and be even more lethal than the first wave of December 2019 to October 2020.

China’s Suppression

China’s actions in suppressing the truth, using the WHO to promote its lies internationally, and expelling independent journalists are all consistent with the actions of someone with something to hid. What was China hiding? What China wanted to hide was not the disease itself; tht was impossible. China was hiding the source of the disease. This was an effort to Deflect responsibiliyt and neutralize trillions of dollars of damage claims. China needed to make the viral spread appear natural and unintended. China went further, using its new “wolf warrior” diplomacy, and blamed the US for releasing the virus. There are two major laboratories in Wuhan that conduct biological research involving bat coronaviruses that could potentially jump to humans. One is the Wuhan Institute of Virology and the other is the Wuhan Center for Disease Control and Prevention. Risky experiments involving genetic engineering using a reverse genetics system on SARS-like virus existing in Chinese horseshoe bats resulted in an artificial virus that could “replicate efficiently in primary human airway cells,” according to a scientific paper coauthored by Dr. Shi Zhengli_Li. Dr. Shi is the director of the Center of Emerging Infectious Diseases at the Wuhan Institute of Virology. Dr. Shi’s work has been heavily criticized by other scientists as involving excessive risk related to potential benefits. In January of 2018, the US embassy in Beijing sent diplomatic able to Wash DC, warning that the Wuhan Institute of Virology “has a serious shortage of appropriately trained technicians and investigators needed to safely operate this high containment laboratory.

The type of bat that carries the lethal coronavirus is not found within a hundred miles of Wuhan. The Lancet published an article on January 24, 2020, that showed 75 percent of the earliest identified cases of COVID-19 in one study invovled individuals who had no prior exposure to the Huanan Seafood Market. Gao Fu, the director of China’s Centers for Disease Control and Prevention, said that he and his team of inspectors examined the Huanan Seafood Market in early January 2020 and found no coronavirus traces in any animal samples tested.

Yes informed parties have not claimed the virus was bioengineered, only that it leaked from a laboratory through negligence. Most virology labs have large numbers of caged animals for experimental purposes. These animals may have had SARS-CoV-2 in a natural form and passed the virus to humans through blood, feces, or contact with other bodily fluids. Saying the virus was not engineered is not the same as sayiung it did not come from a lab. The widely cited article proves nothing with regard to the source of the virus. The study was partially funded by the Chinese government.

There is clear evidence that the Wuhan Institute has live bat coronavirus strains today and has conducted risky experiments involving the possibility of transfer to humans in the past.

This quote is supported by the following video.

Unnecessary Lockdown

The lockdown of the US economy and the end of social intercourse beginning in the stages of March 2020 will be viewed as one of the great blunders in history. The lockdown was unnecessary, ineffectivve and based pon both official deception and bad science. The costs were not considered. Better alternatives were ignored. It was mostly uncontitutional. The lockdown represented rule by experts operations outside their areas of expertise who were revealed to be not that expert even within their fields.

Another rationale for the lockdown was that it would buy time to create a vaccine. The costs of shutting down the economy would be offset by the lives saved once a vaccine was ready for mass innoculations. This would render the virus almost harmless, and the pandemic and allow for a relatively risk free reopening of all facets of the economy. There’s only one problem with this vaccine rationale. An effective vaccine is highly unlikely to appear. Dr. Jay Bhattacharya, professor of medicine at Stanford University, stated the matter succinctly: “There aren’t any vaccines for human coronaviruses…We don’t have a single vaccine for any of them.” Dr. Bhattacharya makes a point that is often lost in the Wall Street chatter and hype about “silver bullets” and “miracle drugs.” SARS-CoV-2 is not a flu virus. COVID-19 is not influenza. We are dealing with a new virus and a mysterious disease we do not understand.

Even a successful vaccine must be judged in the context of a viral mutation. Medicine could create a vaccine that produces antibodies for one version of the virus, only to discover the virus mutated into a more lethal form that is unaffected by those antibodies. Two recent studies, one conducted in China, and the other in Spain, indicate that antibodies produced in those infected with SAARS-CoV-2 may decrease significantly in as little as three weeks. A contributor to the Spanish study, Raquel Yotti, said, “Immunity can be incomplete, it can be transitory, it can last for just a short time.” The implications fo these studies is that even if a vaccine is developed, it may be of limited effectiveness if any antibodies produced disappear within weeks.

Economics aside, there are a host of other costs that argue against a lockdown. The first is immunity loss. While we are all working from home (if we could) to avoid SARS-CoV-2, we were also evading a long list of other viruses and bacteria thta we routinely encounter. Those encounters help us to maintain immunities. By staying in place, our immune systems have now weakened. As we venture out again, those viruses and bacteria will be waiting for us. Many will sicken and die because we have squanered our immunities.

Paul Krugman

Lockdown supporters have attempted to rebut critics by claiming the critics are in effect trading dollars for lives. One of the most outspoken voices for this view is Nobel Prize winning economist Paul Krugman. In a column entitled “How Many Will Die for the Dow?” we wrote, “Trump and his party want to go full speed ahead with reopening no matter how many people it kills….their de factor position is that Americans must die for the Dow.” As an economist, Krugman did some brilliant work in the 1990s. As a columnist, he has been wrong about almost everything since. Policy makers calculate trade offs between potential death and safety and efficiency every day. The point is that these trade offs are made continunually both from a policy perspective and through individual choices. Krugman’s top down, doctrinaire approach is typical of academia and shines a light on bureaucracy’s tendency toward totalitarian solutions.

The Original Sin

The original sin in this entire policy sequence is that Robert Glass, the coauthor of the 2006 paper, was not an expert in disease. He was familiar with complexity models involving what are called “automonous agents” interacting based upon preprogrammed response functions to programmed changes in conditions. The output of Glass’s model was worthless because the assumptions in the models were inflexible adn ignored human behavior. Glass ignored these limitations and developed lockdown models with a rigid, unrealistic set of assumptions. The CDC did the rest. The entire lockdown scenario was based on specifications worked out through the Bush, Obama and Trump administrations based upon a paper produced by a scientist who knew nothing about disease, behavioral psychology or economics.

The lockdown was unnecessary and ineffective. It was the ultimate failure of elite expertise. Alternatives were available. The lockdown was a world historic blunder.

How Long Can a Business Pay Bills from Cash?

How long can a typical business pay its bills from cash balances with no new revenues received? For restaurants, the limit is sixteen days. For retail stores it is nineteen days. For professional services such as lawyers and accountants, its thirty three days. Personal services businesses such as salons an stylistgs can last twenty one days. The mean figure for all small businesses is twenty seven days.

The Long Term Decline in Productivity

Lately, productivity has been declining slightly for reasons economists don’t entirely understand. It may have to do with an aging demographic or the fact that we use technology to waste time instead of getting work done.

Second Wave of Infections

A second wave of infections is not caused by a return of exactly the same virus. It is caused by a mutation or genetic recombination that can create a new variant even more lethal than the original form of the virus. Most assumed that the country would be past the plague by late 2020. There is no certainty in that forecast. A more lethal wave in 2021 is an open possibility.

Depth of the Depression

What is unclear to most observers is that nature and timing of the recovery. The answer is that high unemployment will persist for years and the United states won’t regain 2019 output levels until 2023; growth going foward will be even worse than the weakest ever growth of the 2009 to 2019 recovery. That may not be the end of the world, yet it is far worse than the most downbeat forecasts.

Projections

Based on the most rigorous study available. Our projections of slow growth for several years are too modest. The best evidence points to slow growth for 30 years of March 2020 study entitled longer run economic consequences of pandemics by a Federal Reserve economist in two academics from the University of California, examines the economic impact of pandemics, with at least 100,000 deaths, beginning with the Black Death and 1347, the author, the author’s conclusion states, quote, significant macroeconomic after effects of the pandemics persist for about 40 years, with real rates of return substantially depressed, They go on to say quote pandemics have effects that last for decades. These results are staggering. For context to COVID-19, unquote. For context, the COVID 19 pandemic is on track to cause more fatalities than all but four of the 15 pandemics studied the trade offs between savings and consumption are academic at this point because Americans have already voted with their wallets. In May 2020 US savings as a percentage of disposable income skyrocketed from 7.5% to 33%, Americans were saving not spending this makes sense if you were unemployed and worried about making the next car payment or rent payment. It also makes sense. If you are unemployed yet worry you might be next to get a pink slip. Even if your job and income art are secure. You might save more because of the prospect of deflation in deflation cash can be your best performing asset because the real value of cash goes up as the cost of living goes down. All these elements more layoffs more bankruptcies feedback loops in a spending strike in the form of higher savings mean the recovery will be slow and unemployment will stay high. There will be no V shaped recovery, there are no green shoots despite what you hear from the media. We are in the next great depression and will remain so for years.

Understanding Modern Monetary Theory

Behind these multi trillion dollar deficit and debt monetization efforts called Modern monetary theory MMT which purports to alleviate concerns about debt sustainability. Until recently MMT was a fringe view that some support on the far left today it is the de facto economic law of the land, even if most of the legislators who had tried MMT had never heard of it. We examine MMT monetary policy and fiscal policy as crisis responses in the section below.

None of these policies accomplishes the goals of ending the depression recovering lost jobs and regaining real growth. The, they are empirically and behaviorally valid reasons why these policies will fail. Finally we examine the greatest danger at all, of all deflation and why seemingly unlimited money printing and spending won’t end it there is a cure for deflation, which we explore in the conclusion yet that cure is not in the intellectual toolkit of the central bankers or legislators today. This phrenic void pass presages years of low growth, it is one more reason we face a depression, and not a mere recession and one more reason investors need to be acutely forward leaning to avoid lost wealth, and lost opportunities. The need to spend money in response to the economic shock of COVID-19 has moved modern monetary theory from the fringes of economic policy to a place that centerstage modern monetary theorists such as Bard College professor, l Randall, Ray, W, Ray and investor Warren Mosler offer a curious blend of progressivism and pre Keynesian concept called Shar Taylorism MMT advocates are really small but ascendant clique, who offer the world what the world wants most free money. The two key institutions in the view of the MMT seers, are the Federal Reserve and the US Treasury.

Modern monetary theory has been mana for those members of Congress looking to increase deficit spending by more in one year than the cumulative national debt of every net of every president combined from George Washington to Bill Clinton, Congress doesn’t mind spending money it it needs some sort of intellectual air cover when projected deficits for a single year is over 20% of GDP. Modern monetary theory fills the bill, even if it’s a scholarly snow job, by the time its real world deficiencies come to light that money will be long gone and the American people will be left to pick up the pieces. Modern monetary theory is old wine in new bottles the old wine consists of the belief that the value of money is created by government dictate, and the volume of money is unlimited because government offers citizens no choice but to use their money as payment for taxes, As long as government money is the only medium with which to pay taxes, citizens must acquire that approved form of money to avoid incarceration for tax evasion.

According to Kelton, your money is valuable because the state says so.

Yes, that is actually true, and there are many historical examples of this being true.

From this reasoning Kelton and her ilk expand in all directions if money is what the state says it is, then anything can be money including gold. Prior to the late 20th century, most state money was gold Kelton claims gold was money not because of scarcity utility but because the state proclaimed its money is a matter of custom more than necessity. Once paper became the object of the proclamation paper became money and gold fell by the wayside

Kelton claims a debit and credit are the same things viewed from different perspectives. The state transfers dollars to citizens. The state is a debt or because dollars are central bank liabilities. Citizens are creditors because they accept and hold the debt. This concept that money equals debt allows Kelton to create what she calls a hierarchy of money, literally, anyone can create money in some form by issuing an IOU it’s as if the Federal Reserve expanded its definition of the money supply. It’s all money all credit and all debt at the same time, MMTs intellectual failings will become apparent in the next several years. This can play out as persistent deflation. Because MMT policies cannot create growth or inflation, as MMT policies destroyed confidence in state money, likely both will emerge deflation first followed by inflation. For now, the importance of MMT is not that it works. It doesn’t, but then it provides a cloak of credibility for Congress to spend unlimited amounts and for the Federal Reserve to monetize that spending, both monetary policy and fiscal policy are an overdrive to stimulate the US economy in the face of the new Great Depression. Neither money printing nor spending provides stimulus for reasons explained in the following sections. The academic lip gloss of MMT does not change that result.

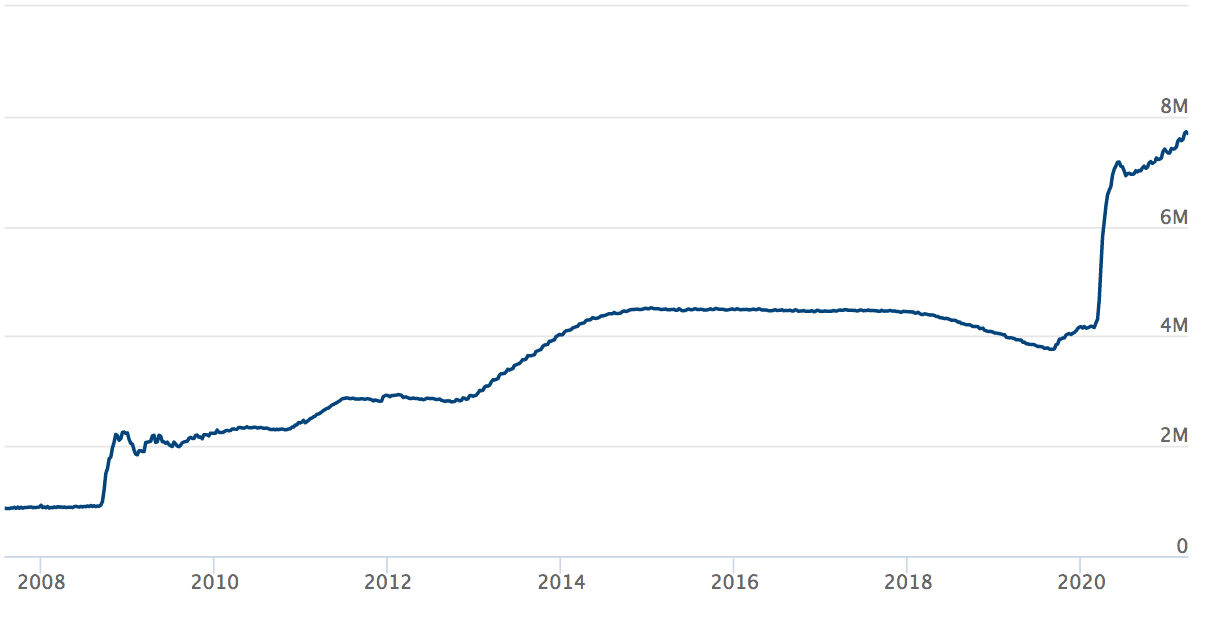

The Fed’s Long Term Failures

Since 2007 The Fed has piled failure upon failure, which eight obscures by making each failure larger than the one before. We’re nearing that the end game. To understand why we need to look at what we’ve where we’ve been, the Fed responds to what became the 2008 global financial crisis began in August 2007 In the aftermath of the failure to Bear Stearns mortgage security, hedge funds in late July, the effective federal funds rate. The policy rate targeted by the Fed fell from 5.262. In July, to 5.02% in August 2007. From there the drop was precipitous and the Fed funds rate hit point one 5% By January 2009 At that point Fed Chairman Ben Bernanke he had no more interest rate ammunition and resorted to money printing under the name of quantitative easing. This came in three waves called QE two and QE three, the effect of the print the money printing was to increase the Fed’s balance sheet from 865 billion in August 2007 At the start of the crisis to over 4.5 2 trillion.

Since this was written, the balance sheet has increased to nearly 8 trillion. This balance sheet information was taken from the Federal Reserve Website.

Quote Continued

In January, 12 of 2015, just after the completion of the QE three taper, which had gradually reduced the amount of new money printing to zero. From there, the Fed kept its interest rates at zero and its balance sheet at about 4.2 trillion until the first interest rate increase on December, 16 2015, the federal funds target increase steadily from 2.5%. On December, 20 2018, and the Fed started to reduce its balance sheet. In November, 2017, under a program called quantitative tightening or QT. This amounted to destroying base money, the Fed reduced its balance sheet from 3.7 6 trillion. By August, to 26th 2019, a $760 billion reduction in assets in less than two years. Analysts estimate that for every $500 billion in reduction, the money supply in the money supply was roughly equivalent to a 1% increase in interest rates. The combination of real rate hikes and effective rate hikes through Qt meant that the Fed was engaged in extreme form of money tightening in 2015 to 18, in what was still a weak economy, of course, the Fed did not understand this due to its deficient forecasting ability. Both the increase in interest rates starting in 2015 and reduction of the balance sheets are starting in 2017 were efforts by the Fed to normalize rates and money supply. The feds goal was to push rates to the 4% level and reduce assets to around 2.5 trillion to prepare for the next recession. If the Fed could normalize it would have enough tripod or in the form of potential rate cuts and money supply increases to fight a recession. The conundrum was whether the Fed could normalize before a recession without causing the recession, it was preparing to fight. My view was always that the Fed would fail and that there was no exit from zero rates, and that a bloated balance sheet, without causing a recession. The Fed did fail stock plunged almost 20% in October 2018 to December, 24 2018, the famous Christmas Eve massacre in response to the Feds tightening the Fed chair, Jay Powell quickly reverse course in late December 2018 Powell first signaled, he would not raise rates further by March 2019 The Fed signaled rate cuts and it followed through on July, 31 2019, with the first of three rate cuts that year. The Fed also announced the end of quantitative tightening a method for reducing the money supply, and began to expand its balance sheet again. Now the Fed has abandoned any pretense of integrity by increasing its balance sheet from 4.2 trillion to 7.2 trillion between March 1 And June of 2020. Additional trillions of dollars of balance sheet expansion were expect are expected in 2021. The Fed is capable of only one task inflating stock market valuations as needed. stock market investors have taken note and respond accordingly, pumping up stock markets is not part of the Feds dual mandate price stability and maximum employment yet. The Fed is good at it.

Why Monetism is Wrong

The difficulty is that none of the programs that the Fed has used for the stock market provide stimulus or create jobs, none of them will return the economy to trend growth, even to the week 2009 to 2019 trend growth, they will keep hedge funds and banks from failing and they will keep trading markets from freezing up in the short term. Yeah, these programs are not a source of jobs or growth. The reason for this world, historic litany of failure by the Fed can be reduced to one word, velocity, that is the turnover of money to explain why a detour, a detour through the theory of monetarism is needed. Monetarism is an economic theory closely associated with Milton Friedman winner of the Nobel Prize in Economics in 1976. It’s basic ideas of changes in money supply, are the most important cause of changes in GDP. The US GDP challenge is measured in dollars are broken into two parts, a real component which produces actual gains, and an inflationary component which is illusionary. The real plus the inflationary equals, then nominal increase measured in total dollars. Friedman’s contribution was to show that increasing money supply in order to increase output would work only up to a certain point, Beyond that nominal gains would be inflationary effect the Fed could print money to get nominal growth yet, there would be a limit to how much real growth would result.

The Velocity of Money is Not Constant

A monetarist attempting to fine tune monetary policy, shows that if real growth is capped at 4%. The ideal policy is one in which money supply grows at 4%, velocity is constant and the price level is constant. This produces maximum real growth and zero inflation. It’s all fairly simple as long as the velocity of money is constant. What if velocity is not constant. It turns out that velocity is not constant, contrary to Friedman’s thesis philosophy is like a joker in the deck. It’s a factor, the Fed can control philosophy psychological depends on how an individual feels about her economic prospects philosophy cannot be controlled by the French printing press. And that’s the fatal flaw in monetarism as a policy tool. Velocity is a behavioral phenomena and a powerful one, the velocity of M to the broad definition of money supply peaked at 2.2 in 1997. That means that for each dollar of money supported 2.2 dollars of nominal growth velocity has been declining precipitously ever since it fell to two.

In 2006 Just before the global financial crisis and then crash to 1.7 in mid 2009 As the crisis had bottom, the velocity crash did not stop with a market crash, the velocity continued to fall to 1.43 by late 2017 Despite the Feds money printing, and the zero rate policy that went from 2008 to 2015. Even before the new pandemic related crash velocity fell to two to 1.37. In early 2020 It can be expected to fall even further. As a new Great Depression drags on, when consumers pay down debt and increase savings instead of spending velocity drops as GDP, unless the Fed increases the money supply. The Fed is printing money prodigiously to maintain nominal GDP in the face of declining velocity, a problem that has not faced since the 1930s as velocity approaches zero, the economy approaches zero as well, money printing is impotent 7 trillion times zero equals zero. If the money expansion mechanism is broken because banks will not lend and velocity is declining because of costs consumer fears, then it’s impossible for the economy to grow. There is no economy without velocity. This brings us to the crux, the factors the Fed cannot control such as base money are not growing fast enough to revive the economy and decrease unemployment. The factors that the Fed needs to accelerate our bank lending and velocity in the form of spending spending is driven by the psychology of lenders and consumers essentially a behavioral phenomena. The Fed has forgotten if it ever knew the art of changing expectations without inflation, which is the key to changing consumer behavior, and driving growth. It has almost nothing to do with money supply, contrary to the nostrums of the monetarist and the Austrian School economists.

John Maynard Keynes and Deficit Spending

The idea that deficit spending can stimulate on otherwise stalled economy dates to John Maynard Keynes and his classic work. The General Theory of Employment, Interest and Money from 1936 Keynes’s idea was straightforward he considered output a function of what he called aggregate demand. This is usually driven by business and consumer demand at times. This demand was lacking because depression airy conditions or deflation drove consumers into a liquidity trap in this condition consumers prefer to save rather than spend, both because prices were falling and because the value of cash was going up in those conditions it’s smart to defer buying and increase savings gains the solution is to the liquidity trap was to have government step in with government spending to replace the individual spending deficits were a perfectly acceptable way to do this in order to break the back of deflation and revive what Keynes called animal spirits. Keynes went further and said that each dollar of government spending could produce more than $1 or growth. When the government spent money or gave it away, the recipient could spend it on goods and services, those providers of goods and services would in turn pay their wholesalers and suppliers which would increase the velocity of money depending on the exact economic conditions, it might be possible to generate 1.3 dollars of nominal GDP for each dollar of deficit spending. This was the famous Keynesian multiplier, to some extent the deficit would pay for itself in increased output and increased taxes. In practice, Keynes’s theory was not a general theory but a special theory, it would work only in limited conditions. It worked when the government started in a depression, or in the early stages of recovery. It worked when the initial level of government debt was low and sustainable. It worked in conditions of deflation and a true liquidity trap. Keynes was not an ideologue he was a consummate pragmatist, his prescription was the right one for the 1930s.

Paul Samuelson Distorted Keynsiansim?

Unfortunately his ideas were grossly distorted. After his death, by Paul Samuelson and his followers at MIT and other centers of economic thought Keynes’s limited solution was turned into an all purpose prescription that deficits, could be used to promote growth at all times and an all places, provided the spending is aimed at social goals, approved by the academic elites MMT is the read reductor ad absurdim of what came from MIT, the belief that deficit spending of any quantity at any time produces more growth than the amount spent, is what lies behind the claims of stimulus in the congressional frenzy of trillion dollar deficits now wonder why this is a false belief.

In fact, America in the world are inching closer to what Carmen Reinhart and Ken Rogoff, described as an indeterminant yet real point, when an ever increasing debt burden triggers creditor revulsion forcing a debtor nation into austerity outright default or sky high interest rates, the creditor revulsion point where more debt does not produce commensurate growth due to lost confidence in the debtors currency is reached as follows the country begins with a manageable debt to GDP ratio commonly defined as less than 60% in search for economic growth, perhaps to emerge from a recession or simply buy votes. Policymakers start down a path of increased borrowing and deficit spending. Initially results can be positive, some Keynesian multiplier may apply. Especially if the economy has under utilized and just industrial and labor force capacity, and assuming the borrowed money is used wisely in ways that have positive payoffs. Over time, the debt to GDP ratio pushes into a range of 70 to 80%, the political constituencies developed around the increased spending the spending itself becomes less productive more spent on current consumption in the form of entitlements benefits and less fruitful public amenities, community organizations and public employee unions, the law of diminishing marginal return starts to bide yet the the public’s appetite for deficit spending, and public goods is insatiable the debt to GDP ratio eventually pushes past 90%. The Reinhart and Rogoff research reveals that a 90% debt to GDP ratio is not just more of the same, rather it’s what physicists call a critical threshold at which a phase transition occurs, the first effect is that the Keynesian multiplier falls below one, the dollar of debt and spending produces less than $1 of growth, no net growth is created by added debt while interest on the debt increases the debt to GDP ratio on its own.

This Research Has Been Discredited As There Was a Spreadsheet Error

Today pandemic related debt creation is not an incremental it’s exponential relative to prior deficits and it comes at a time when the GDX the debt to GDP ratio is already well past the Reinhart Rogoff 90% line. Creditors grow anxious when continuing to buy more debt in a vain hope the policymakers will reverse course or growth will spontaneously emerge to lower the ratio.

The United States is the best credit market in the world and borrows in a currency and prints. For that reason alone, it can pursue an unsustainable debt dynamic longer than other nations, yet history shows there is always a limit, the salience of the Reinhart-Rogoff research is not the eminence, or default, but the weight of the structural headwinds to growth. Of particular importance to the United States is the Reinhart Rogoff paper debt and growth revisited from 2010, the author’s maintain conclusion is that debt to GDP ratio is above 90%. The median growth rates fall by 1% and the average growth rate falls considerably more importantly Reinhart and Rogoff emphasize that the importance of nonlinearities in debt growth for debt to GDP ratios below 90% There’s no systematic relationship between debt and growth. Put differently, the relationship between debt and growth is not strong at lower ratios. Other factors including tax monetary and trade policies all guide growth. Once the 90% threshold is crossed debt is the dominant factor above 90% debt to GDP an economy goes through the looking glass into a new world of negative marginal returns on debt, slow growth and eventual default through nonpayment inflation or renegotiation. The point of default is sure to arrive yet it will be preceded by a long period of weak growth stagnant wages rising income inequality and social discord a phase where dissatisfaction is widespread, yet no dental ma occurs. Other research, respected research reaches the same conclusion. Reinhart and Rogoff may have led the way in the field but they are not out on a limb evidence is accumulating that developed economies, in particularly the United States are on dangerous ground, and possibly past a point of no return. The end point is a rapid collapse of confidence in the US debt and the US dollar. This means higher interest rates to attract investors to continue financing the debts.

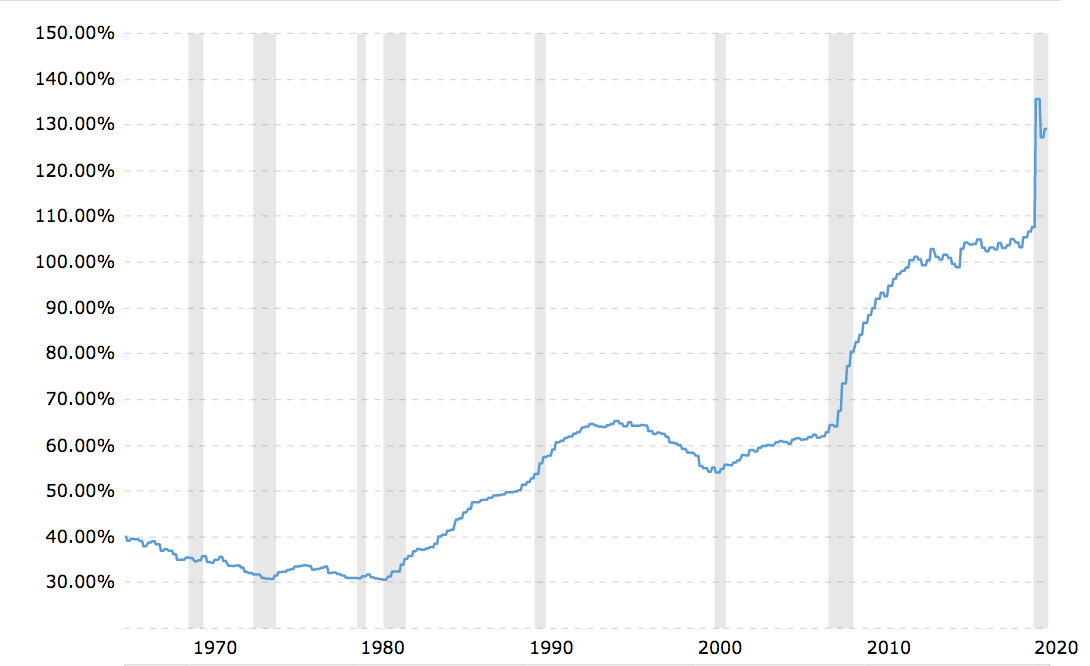

The coronavirus stimulus has caused the debt to GDP ratio to reach unprecedented levels and sits at roughly 130%.

Debt to GDP Ratio Historical Chart

The all-time high for the previous debt to GDP ratio was in 1946 and that was right after WW2. This was a complete wartime economy and mobilization. It does not make any sense that the US debt to GDP ratio would be anywhere close to this during a pandemic. Furthermore, this 118% level of debt dropped to 92% two years later, even though the country was in a recession. The US economy did not take off in the post-war period until 1950. The debt to GDP ratio was in the low 30s all through the 1970s. It hit 40% or above in the 1980s and never declined since that time. The next major inflection point was 2009 in response to the Great Recession of 2007-2008.

What should be noted was that the US debt to GDP ratio was already at 106% before the coronavirus hit and the US engaged in the stimulus.

However, the public debt to GDP ratio is not a predictor of anything and could be immediately eliminated tomorrow by having the private central bank (the Fed) converted into a public central bank and removing private banking interests from central banking, and having the government create its own money.

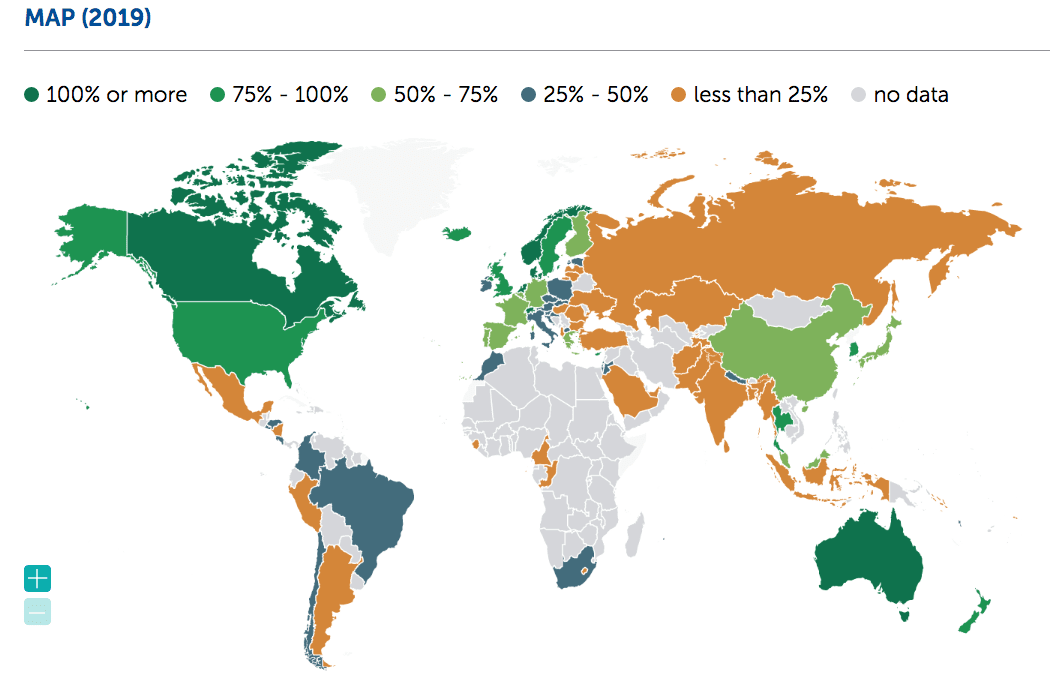

Another major topic of discussion is the personal debt to GDP ratio.

The US personal debt + the government debt is high. It is around 4x the US GDP. However, low personal debt is not a feature of successful economies. This graphic shows the personal debt percentage of GDP. Notice that the more well-off countries have a HIGHER debt to GDP ratio, not lower. (graphic from the IMF)

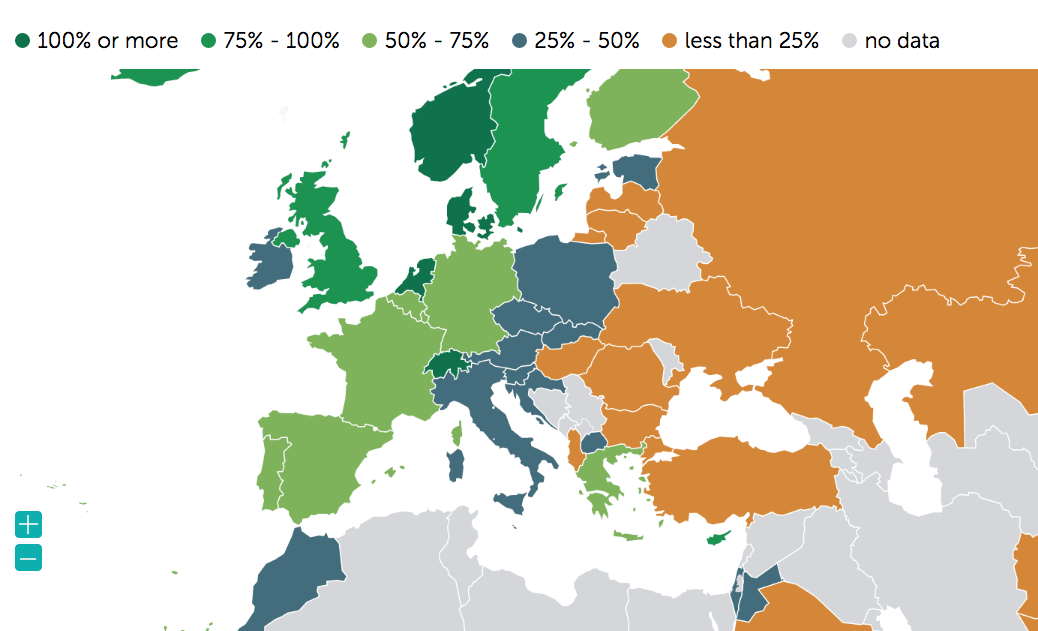

Notice the strong distinction between Western Europe, Central Europe, and Eastern Europe. It is small, but if you focus on it, you can see it clearly. Let us zoom in.

This is the zoomed-in view. The debt to GDP ratio is positively correlated with the level of the economy.

What is curious is that the least developed countries don’t have any data on the debt to GDP ratio at all. And this is from the IMF. Why is there so little data? Africa has almost no data on this metric. However, overall their debt to GDP is low. But that is not a good thing.

This is sort of the problem with stating that the high total debt to GDP ratio is bad. Looking at all of the countries, what is the optimal debt to equity ratio. It is not at all clear looking at the list of countries and reading each debt to equity ratio.

The relationship between private debt and the economy is explained in the following quotation from Richard Vague.

What’s astonishing is how little attention the global debt problem—the extremely high ratio of private debt to GDP—has gotten. Not only does it leave the U.S. and other countries vulnerable to crisis should brisk growth in that ratio resume, but, quite apart from any crisis, the accumulation of higher levels of private debt over decades impedes economic growth. Money that would otherwise be spent on things such as business investment, cars, homes, and vacations is increasingly diverted to making payments on the growing debt— especially among middle- and lower-income groups that compose most of our population and whose spending is necessary to drive economic growth. Debt, once accumulated, constrains demand.

The ideal condition for growth is to have less capacity (that is, the supply of housing, factories, etc.) than demand, coupled with low private debt. This was the case during the decades immediately after World War II. But now we have nearly the opposite situation. In the first decade of the 2000s, the United States and Europe built far too much capacity, especially in housing, and incurred too much private debt. In the 1980s, Japan built far too much capacity, saddling its banks with too much private debt and too many bad loans. While all these countries have been catching up to this capacity, none yet has less capacity than demand, and all still have high private debt. And now China, whose industrialization and urbanization long fueled global growth, has created its own overcapacity and private debt problem, building far too much capacity in the form of industrial and real estate projects while providing easy credit that fueled a rapid buildup of private debt. So no major global economic player now has that pivotal combination of undercapacity and low private debt that can fuel productive investment and help boost global growth.

What’s more, excessive private debt may contribute to one of the great problems of our time: growing income inequality and the hollowing out of the middle class. The middle class tends to grow when there is too little capacity and low private debt (as after World War II). In contrast, the middle class plateaus or shrinks when there is too much capacity and too much debt (as at the present). Stated differently, inequality increases when there is high capacity and high debt; it decreases when capacity and debt are low.

The Results

The result is another 20 years of slow growth austerity and financial repression, where interest rates are held below the rate of inflation to gradually extinguish the real value of debt, and an expanding wealth gap, the next two decades of US growth will look like the last three decades in Japan, not a collapse just a long slow stagnation another name for depression. Modern monetary theory is an intellectual sham that celebrates the coercive power of the state and fails to credit the importance of confidence in the operation of monetary systems, monetary policy fails because it ignores the behavioral root of velocity relying on money creation and not comprehending while people refuse to spend money, Even when it’s offered up by the truckload.

US debt is at a point where no feasible combination of real growth and taxes will finance repayment of the real amount owed. If the Fed can cause inflation slowly at first to create money illusion and then more rapidly the debt will be manageable because it will be repaid in less viable nominal dollars in deflation the opposite occurs the real value of debt increases making the repayment more difficult. The second problem with deflation is its impact on the debt to GDP ratio. This ratio is a debt amount divided by the amount of GDP, expressed in nominal terms. debt is continually increasing in nominal terms because of continual budget deficits that require new financing and associated interest payments.

The new great depression will be characterized by powerful deflation, at least initially this deflation will be the result of greatly increased savings reduce spending and falling money velocity, lower prices will beget more savings, which will be get lower prices and so on in a classic liquidity trap and deflationary spiral workers who have lost their jobs, businesses that have shut their doors and others who fear they will be next to suffer the same fate will be in no mood to borrow or spend.

Ultimately, the psychological impact of a pandemic will harm far more people than the virus itself, and the widespread emotional trauma it’s invoking will be long lasting. Experts say already more than four in 10 Americans say that stress related to the pandemic has had a negative impact on their mental health. There’s no doubt that the Coronavirus pandemic will be the most psychologically toxic disaster in anyone’s lifetime says George Everly who teaches at the John Hopkins Bloomberg School of Public Health.

A growing body of research reports result, consistent with those described above, while in its early stages what medical studies reveal are distinct neurological and mental health problems emerging from the COVID 19 pandemic. The first relates to invasion of the brain tissue by the virus with complications ranging from severe inflammation and death to more mild yet serious disorientation and cognitive impairment. These conditions are comparable to those resulting from acute infections of the Spanish flu. The second category is not limited to those infected by the virus but it applies to infected and uninfected alike. This has to do with anti social and sometimes violent behavior, as well as depression and anxiety from the response to the pandemic.

Price earnings ratios for the S&P 500 stocks are at levels not seen since the early 2000s dot com bubble the first time, retail investors are cashing IRS bailout and checks and opening online brokerage accounts to buy hurts the company already in bankruptcy.

There’s a myth that markets are efficient venues for price discovery that smoothly process incoming information and adjust continually to new price levels before investors can catch up and take advantage. This has never been true and it’s less true than ever before. This efficient market hypothesis was an idea dreamed up by the faculty lounge at the University of Chicago in the 1960s that has been propagated to generations of students ever since it has no empirical support, it just seems elegant in closed form equations, markets are not are not efficient, they freeze up at the first time in trouble, they do not move continuously between price levels. They gap up or down in huge percentage leaps. This can produce windfall profits for long or wipe out losses for shorts. That’s life. Just don’t pretend it’s efficient, most important, the efficient market hypothesis was used to hurt investors into index funds, exchange traded funds, and passive investing based on the idea that you can’t beat the market so you might as well go along for the ride. That works for Wall Street wealth managers just simply collect fees on account balances and new products. It does not work for investors who take 30% losses or worse every 10 years or so and have to start over to rebuild lost wealth, you can beat the market using good forecast market timing and a perfectly legal form of insight information. That’s what pros do. That’s what robots do, and every investor can do it too.

The Models

Word on models I have been extremely critical of most economic models for years, models such as the Phillips Curve, the Nyro the R star, the wealth effect, Black Scholes, the risk free rate and others are junk science. They bear no relationship to reality there, they are a leading cause of the gap between perception and reality. That leads to periodic shocks, when reality breaks down the door of the faculty lounge. These models which go under the name of dynamics gut stochastic general equilibrium or DSGE model should be scrapped, they won’t be because three generations of academic economists have too much time and effort invested in their creation and perpetuation. That’s okay the academics losses is your gain if policy is guided by flawed models and you know the flaws you can front run the policy. When you make investment decisions, remember you’re not competing with other investors you’re competing with robots. That’s good news because these robots are dumb. They do exactly what they’re told, when you hear the phrase artificial intelligence, you should just count the word intelligence and focus on the word artificial robots are program with code developed by engineers in Silicon Valley, many of whom have never set foot on Wall Street. They use large datasets correlations and regressions, and they read headlines and content for keywords then certain keywords are encountered. And when price action deviates from a pre determined baseline the robot is triggered and executes a buy or sell, that’s about it. Once you understand the robot algorithms, it’s easy to front run them robots assume the future resembles the past, it doesn’t. Human nature may not change yet conditions change all the time. That’s why we have history, robots assume that people who utter the key words know what they’re doing, but they don’t. The Fed has a worst forecasting record of any major economic institution, the IMF is no better official forecast should always be listened to and never relied upon the officials in charge have no idea what they’re doing. The robots massive databases may have a huge volume of data but they don’t go back very far in time, 20 or 30 years is not enough to form a good baseline 90 years is better 200 years is better still, robots routinely buy the dips, Chase momentum and believe the Fed, when you know that robots are leading markets over a cliff, you can front run the inevitable correction and profit from the robots blindspots once again you profit from profit from the gap between reality and perception as fourth quarter 2020 data emerges and as the reality of slow growth rising bankruptcies non performing loans and persistent high unemployment and deflation are taken into account stocks will fall back to Earth and the perception to reality gap will close the improved models project, the Dow at 16,000 and the S&P 500 at 1750.

This has not happened. As of April 7th 2021 the Dow is at 33,440. The S&P 500 is at 4007. This author underestimated the Fed’s ability to stimulate not the economy, but the financial markets. However, the question is how much longer the financial markets can stay untethered to the overall economy.

Quote Continued

By late 2021 with some outperformance in the defense natural resource and technical sectors shares a well run gold mining firms are likely to produce 2,000% gains over the same time period, with a six month lag to advances in the bullion price, physical gold bullion will move from 2000 per ounce past 2500 per ounce. By early 2021 From there further gains to 14,000 per ounce by 2025 or likely this will produce 700% gains over the next four years.

Despite costs in terms of lost social interactions, the benefits in terms of reducing need for high cost prime office real estate in major cities was obvious extensive reductions in demand for corporate office space will result.

Considering Cash

Cash is the most underrated asset class in the mix. This is a mistake by investors because cash will be amongst the best performing asset classes for the next two to three years. The reason cash is disparaged because it has a low yield. That’s true. The yield is close to zero, yet the truism misses several points, the nominal Euro yield may be zero, yet the real yield can be quite high in a deflationary environment. If you have $100,000 in the bank with zero yield, your nominal yield is zero. But if we experienced a 2% deflation during a one year holding period the real yield is 2% the cash amount is unchanged, the purchasing power of that cash has risen by 2%. Another underrated advantage of cash is optionality. When you make an investment it may work or it may not, but either way, there’s a cost to exit if you want to reallocate your assets. At a minimum, you will pay brokerage commissions across the bid offer spread or both. In the case of an illiquid investment such as private equity real estate or a hedge fund, you may not be able to exit at all for several years. In contrast, cash has no exit fee. If you have it you can be the Nimble investor who can respond on short notice to an investment opportunity, others may have overlooked or have not seen coming, cash is your call option on every asset class in the world, optionality has value that most investors don’t understand. Still, it’s real and adds to the value of your cash hoard finally cash reduces your overall portfolio volatility, the nominal value of cash is unchanged in all states of the world, a diversified portfolio contains volatile assets including stocks gold’s and bonds, cash reduces portfolio volatility compared to the volatility of those separate asset classes. Functionally, it’s the opposite of leverage, which increases portfolio volatility.