The Hold Duration For a Sample of Investment Vehicles

Executive Summary

- This article evaluates several investment vehicles to test how long they should be held during periods of increase.

Introduction

We found something interesting regarding when the gains occur with investment vehicles (stocks, ETFs, etc..) that impact the logic of the buy and hold strategy.

*Note

This article is only part of our internal analysis of investing and communicates with people we know. We are not writing this to attract investors, and we are not giving investment advice. This is just a convenient way to document our analysis, which can be easily shared and easily updated.

Setting the Measurement At The Appropriate Level of Granularity

Hold Duration

We decided to review several symbols of investment vehicles to determine how long should they be held to maximize returns.

Judgment Call on Measuring Rally Duration or Length

This is the number of days in a row where the IV has appreciated. This seems simple, but it is not. This is because if one stops counting the rally when there is a slight decline, one ends up with a large number of very short rallies. These rallies are so short they are difficult to “catch.” Some rallies either flatline or decline slightly. However, these flatlines or declines are not relevant to the ROI of the investment. We will show this in the following symbol.

Symbol FCG

This is what the rallies look like if we count the rally as ending as soon as there is a flatline or a decline. This measurement begins in Feb of 2020.

7 14 12 7 2 2 8 3 1 2 2 1 1 6 6 2 5 3 1 3 6 5 1 2 3 2 1 2 1 4 1 4 4 2 2 5 4 1 2 2 2 1 1 3 2 2 4 2 6 5 4 1 3 4 2 2 1 2 1 3 2 5 2 5 1 3 2 3 5 4

Notice the longest rally in this list is 12 days and there are 72 rallies. But the majority of rallies are much shorter. As it takes roughly 3 days to identify a rally, this would mean one would only be able to “catch” around 15 rallies, and then one would need to sell this IV quickly. This is not a tenable investment strategy.

This is what the FCG rallies look like when we count rallies in the following way.

The volatility of this IV of 2.76%

Rule #1

A rally as including some flatline periods and some periods of modest declines. To measure this one needs a rule for what stops a rally. And our rule is a decline of 10% from the high.

This is also our sell signal. However, this also removes some IVs from our selection. Which is fine. This excludes high price variable IVs. This is because a high price variable means shorter rallies and more losses when the IV declines.

We found two IVs with the EGLE that had this issue, so we stopped measuring their rallies. The volatility of EGLE was 4.35%. We don’t consider IVs with volatility score higher than 2.8%

This is therefore another rule inherent in this rule that we want IVs that we can buy and will not frequently trigger us to exit the IV. Every IV that we decide to purchase must have a low enough price variance to allow it to be held for long periods.

Rule #2

If a rally is 2 days or less, we don’t count the activity after those two days. And this is a connected rule. This also matches the fact that we don’t look to buy an IV until it has three days in a row of increases.

Rule #3

Do we buy an IV that has had a 2-day rally and then flatlines? The answer is no. That is we count rallies that our rules state that we would buy into. This means we don’t count many of the rallies, as they are not relevant to us.

These rules completely change the duration of the rallies and also exclude most of the rallies from being counted.

This is what the FCG rallies look like when this rule is applied.

40 35 45 15 37 9 10 64 90 37 12

This brings the number of rallies down to 11 from 72. And it increases the average duration to 35.82. That makes each rally easier to catch and therefore to benefit from. And all it takes is accepting some flatline period and a reduction of 10% from the peak to extend the duration.

We will continue with other symbols. As you will see, FCG is not our idea IV due to its larger than an average number of rallies, and its corresponding relatively low rally duration.

Other Symbols

All of these symbols begin in Feb of 2020.

IGE

75 27 10 219 210

This is a perfect IV. It has only had five rallies in its history (since Feb 2020), and these rallies are mostly quite long. This is the type of IV that is held more than it is not held.

The volatility of this IV of 1.64%

MKL

20 25 25 47 14 80 155 115

This is another suitable IV with eight rallies. Only one of its rallies is at 14 days or lower.

The volatility of this IV of .99%

FTXN

47 240 60 90

This symbol has 4 long rallies.

The volatility of this IV of 2.03%

ESLT

400

The volatility of this IV is .92%

CORN

180

The volatility of this IV is 2.49%. This is a curious scoring for the beta, as the price history looks much more predictable than this.

COWZ

660

The volatility of this IV is 1.63%.

DBA

540

The volatility of this IV is 1.79%.

DHS

630

The volatility of this IV is .67%.

FTXN

450 180

The volatility of this IV is 2.03%.

FXN

630

The volatility of this IV is 2.0%.

HAL

420 105

The volatility of this IV is 2.28%.

JHME

375 180

The volatility of this IV is 1.6%.

XME

300

The volatility of this IV is 2.80%.

The stats below here have yet to be updated.

PALL

165

The volatility of this IV is 2.80%.

Statistics

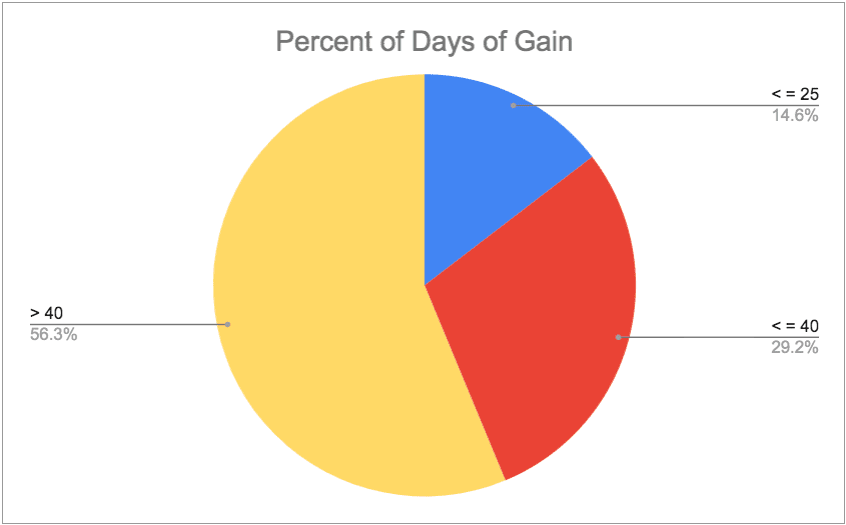

The average duration of gain from these 28 data points of intervals of gain was 66.18 days.

This shows the average number of consecutive days of gain or rally. Only 14.6% of the rallies are less than 25 days. 29.2% are less than or equal to 40 days. And 56.3% are greater than 40 days. To reiterate, to have such long average rallies, one must be selective about what IVs are added to the “basket” of eligible IVs.