What is the Real The Reason for The Fed’s 2% Inflation Target?

Executive Summary

- The US has a very consistent inflation level.

- The logic given for the inflation level is not the real reason for this level of inflation.

Introduction

If you study business in the US, you are taught that inflation is set to optimize the unemployment level. However, this can’t be true, as the US government has already so rigged the unemployment number, mostly excluding individuals, that this can’t be the actual reason.

Getting Realistic About Who the US Government Cares About

The US Government cares about the impression of unemployment (which is why they have put so much effort into rigging the measurement). However, they don’t actually care about the workers in the country. Time and again, it has been shown through policies that the US Government cares about large corporations. This is why it is highly suspicious when an overall benefit to the population is used to explain why the inflation target is set as it is.

This explanation for the inflation target is on the Federal Reserve (not part of the US Government by the way) website.

What the Federal Reserve Says About Inflation Targets

The Federal Reserve has not established a formal inflation target, but policymakers generally believe that an acceptable inflation rate is around 2 percent or a bit below.

Four times per year, Federal Open Market Committee (FOMC) participants–that is, the members of the Board of Governors and the presidents of the Federal Reserve Banks–make projections for how they expect the prices of goods and services purchased by individuals (known as personal consumption expenditures, or PCE) to change over the longer run.

However, why is it 2 percent? The Federal Reserve web page does not say.

And it is not only the Federal Reserve. The Bank of England has the following to say about its inflation target.

To keep inflation low and stable, the Government sets us an inflation target of 2%. This helps everyone plan for the future.

If inflation is too high or it moves around a lot, it’s hard for businesses to set the right prices and for people to plan their spending.

But if inflation is too low, or negative, then some people may put off spending because they expect prices to fall. Although lower prices sounds like a good thing, if everybody reduced their spending then companies could fail and people might lose their jobs.

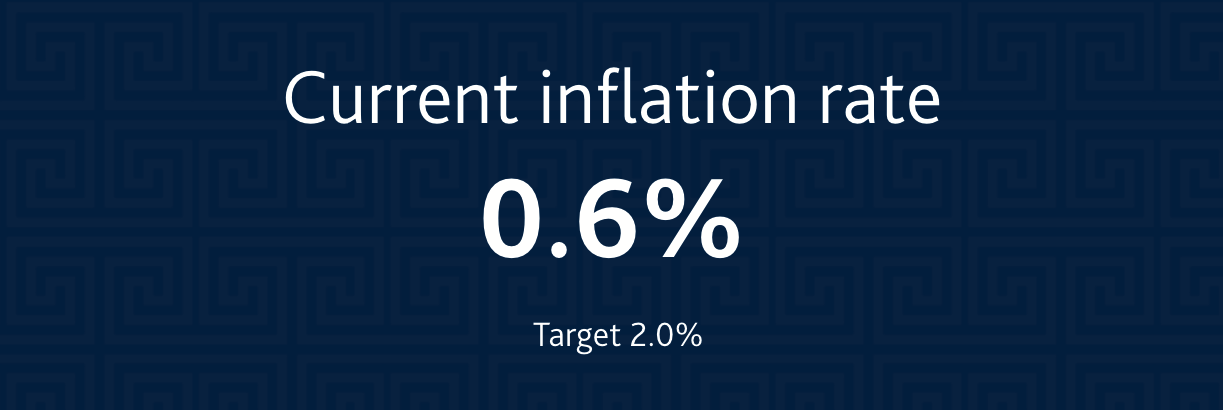

This still does not explain why the level is set at 2%. The Bank of England publishes the current inflation rate versus the target.

One can see that the current inflation rate in the UK is .6% though its target is 2%.

The Long Term Results of Inflation

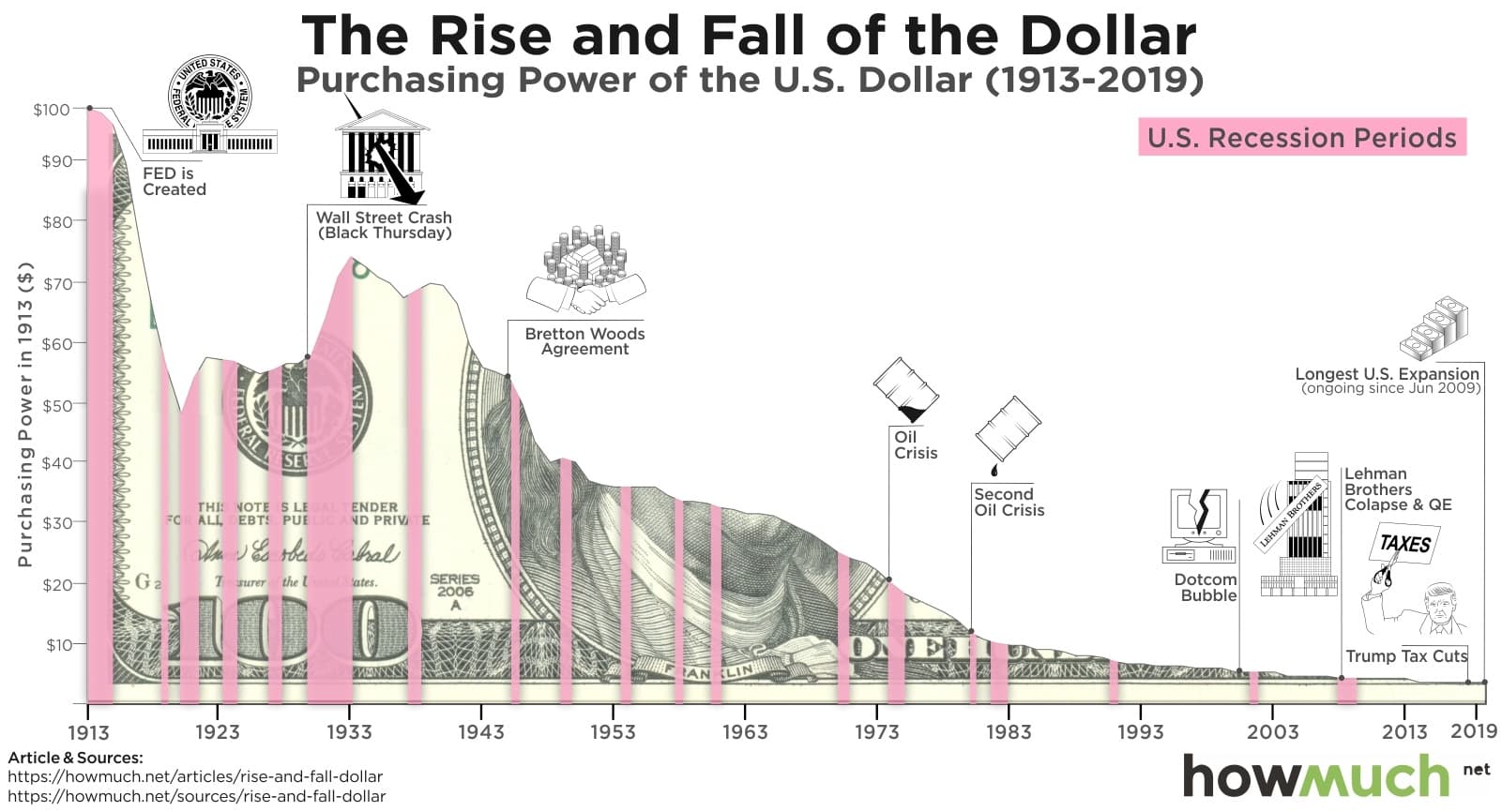

While a 2% inflation rate sounds small, over long periods of time, it has a very strong effect on the purchasing power of a currency.

This graph looks ridiculous. The US government can see this same graph. Why does the US have a policy to erode its currency?

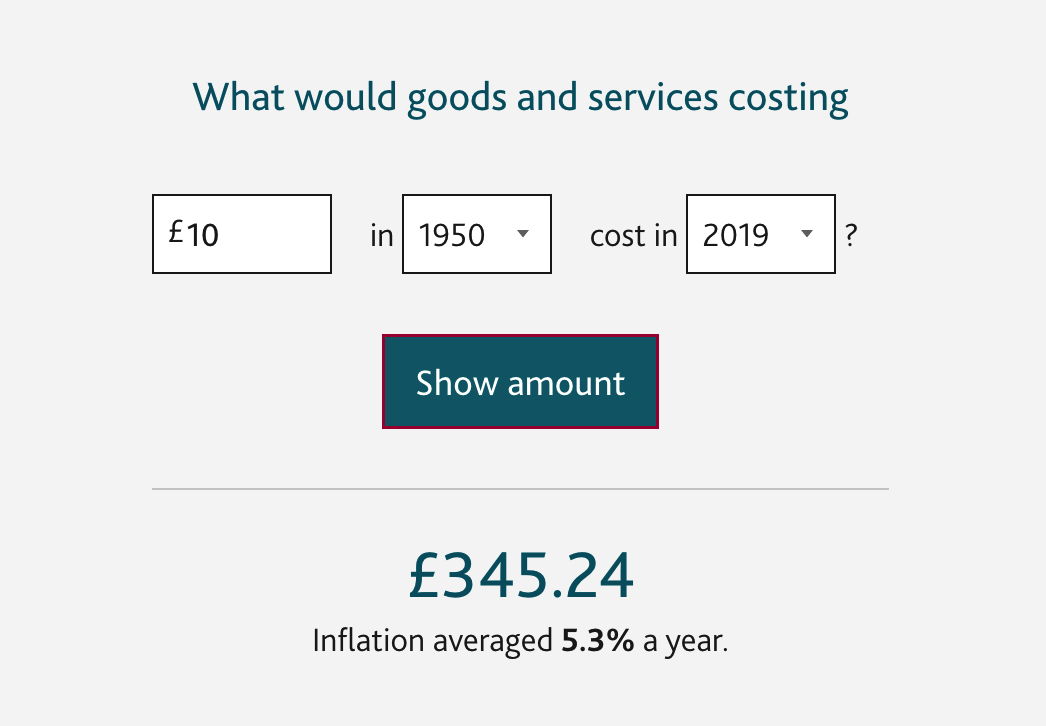

This image shows a shorter time frame and is a little easier to see.

This is covered by Wikipedia in the following quotation.

Over time, the compounded effect of small annual price increases will significantly reduce a currency’s purchasing power. (For example, successfully hitting a target of +2% each year for 40 years would cause the price of a $100 basket of goods to rise to $220.80.) This drawback would be minimized or reversed by choosing a zero inflation target or a negative target.

However, policymakers feel the drawbacks are outweighed by the fact that a positive inflation target reduces the chance of an economy falling into a period of deflation.

That seems to be a hypothesis. But why would an inflation rate target of 0% place the economy into a deflation? 0% is not a deflation. Secondly, isn’t a highly stable currency over decades a robust positive factor? Doesn’t as close to possible to 0% inflation improve planning and stability?

Losing on Retirement Money, Unless You Place the Money at Risk

The problem is that the interest rate in the US on savings of around .09%.

This is functionally 0%. This means that unless you put your money at risk, in the stock market, bond market, into other investments, you lose a little value every year and a lot of value over a long period of time. What is curious, which is barely discussed in the US, is why don’t banks at least pay individuals the inflation rate so that they don’t lose their money?

This is another clue that the Federal Reserve and US Government do not care about most of the population as neither the Federal Reserve nor the US Government mandate that people do not lose the value of their money through inflation.

This is the explanation as to the inflation target from Knowledge at Wharton.

On the other side, a low inflation rate is often associated with economic weakness and nullifies some of the effect of monetary policy meant to stimulate the economy. Low inflation can lead to lower interest rates because when issuing loans or bonds, lenders will demand a premium to account for inflation. When interest rates are low, the Fed will often reduce the benchmark interest rate in order to encourage spending, consequently boosting the economy and preventing economic weakness. As the benchmark interest rate gets very low and even approaches the zero lower bound, however, the Fed becomes increasingly powerless; they can no longer lower interest rates and expansive monetary policy becomes relatively useless and unfeasible.

This does not at all sound like a legitimate explanation, and more seems like a rationalization that someone came up with to justify a predetermined conclusion.

Also, why is the only way described to stimulate the economy the interest rate? There are plenty of ways to stimulate the economy, including deficit spending. As I write this, we are experiencing a decline in economic activity due to the Coronavirus. Lowering interest rates will not stimulate the economy as the demand is not there. The government would need to engage in deficit spending. One good candidate is infrastructure projects, as the US also has a very large backlog of infrastructure that is overdue for maintenance. However, for a number of years, the US has been putting off its infrastructure maintenance.

Knowledge @ Wharton Admits It Does Not Know

In an article about why inflation is set at a particular level, one might expect it to be explained if the author knows. But apparently, this is too much to ask. See this quotation.

Overall, explaining exactly why the inflation rate is 2% is difficult, but the choice is not arbitrary. The number serves as an anchor for people and the fundamental reasoning was to provide the public with a stable and predictable indicator of economic strength. Therefore, even with some fresh arguments for raising the inflation rate gaining prominence, the target inflation rate is likely to remain at 2% for the foreseeable future.

Well, that is good to know. It is not arbitrary! Well, then what is the reason? Is it some type of secret?

The History of the 2% Inflation Target

In a historic shift on 25 January 2012, U.S. Federal Reserve Chairman Ben Bernanke set a 2% target inflation rate, bringing the Fed in line with many of the world’s other major central banks.[24] Until then, the Fed’s policy committee, the Federal Open Market Committee (FOMC), did not have an explicit inflation target but regularly announced a desired target range for inflation (usually between 1.7% and 2%) measured by the personal consumption expenditures price index. – Wikipedia

This illustrates that there is an international consensus that the inflation target should be 2%, and the US came in line with this. But we still do not know why this was the consensus.

Deflation = Depression?

Throughout the explanations, there is an implied tie between deflation and depression. However, this link is not established as strong. Naturally, if there is less demand, then prices decline — but it is not the declining prices that cause lower demand. This should be very obvious as a confusion of cause and effect.

In the study Deflation and Depression: Is There an Empirical Link?, by the Federal Reserve Bank of Minneapolis, the following was found.

There are 65 episodes of deflation without depression and 21 of depression without deflation. Thus, 65 of 73 deflation episodes had no depression, and 8 of 29 depression episodes had no deflation. What is striking is that nearly 90% of the episodes with deflation did not have depression. In a broad historical context, beyond the Great Depression, the notion that deflation and depression are linked virtually disappears.

That sounds like a very poor relationship. And the study says so in the following quote.

The data suggest that deflation is not closely related to depression. A broad historical look finds many more periods of deflation with reasonable growth than with depression and many more periods of depression with inflation than with deflation. Overall, the data show virtually no link between deflation and depression.

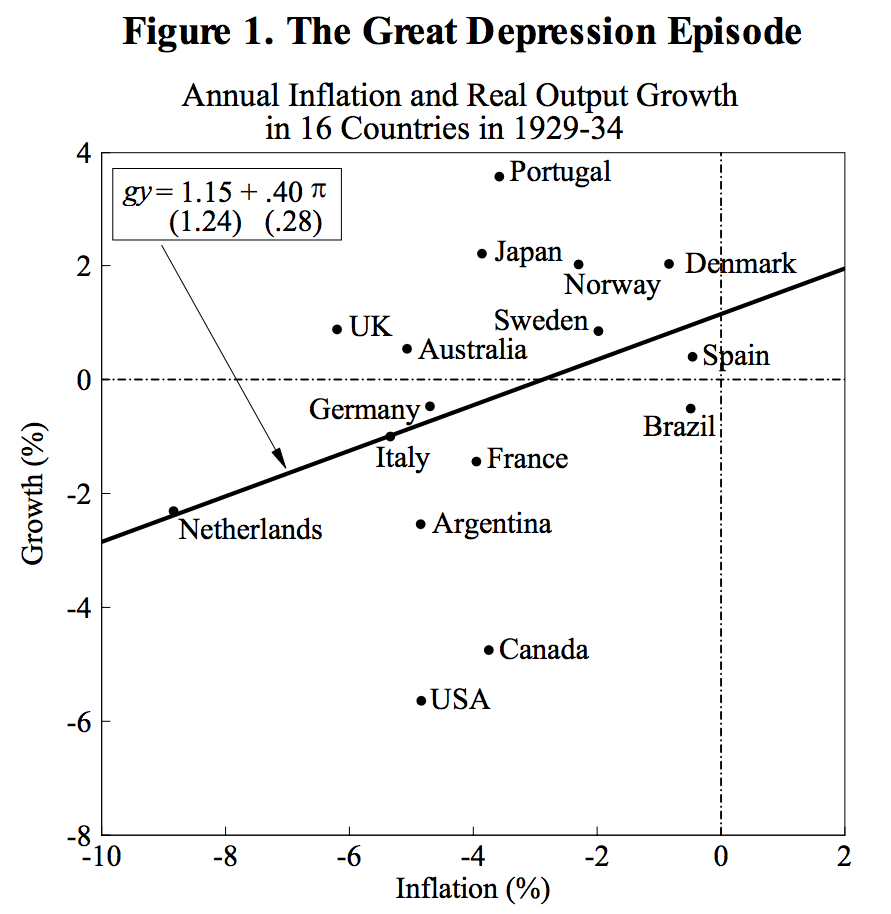

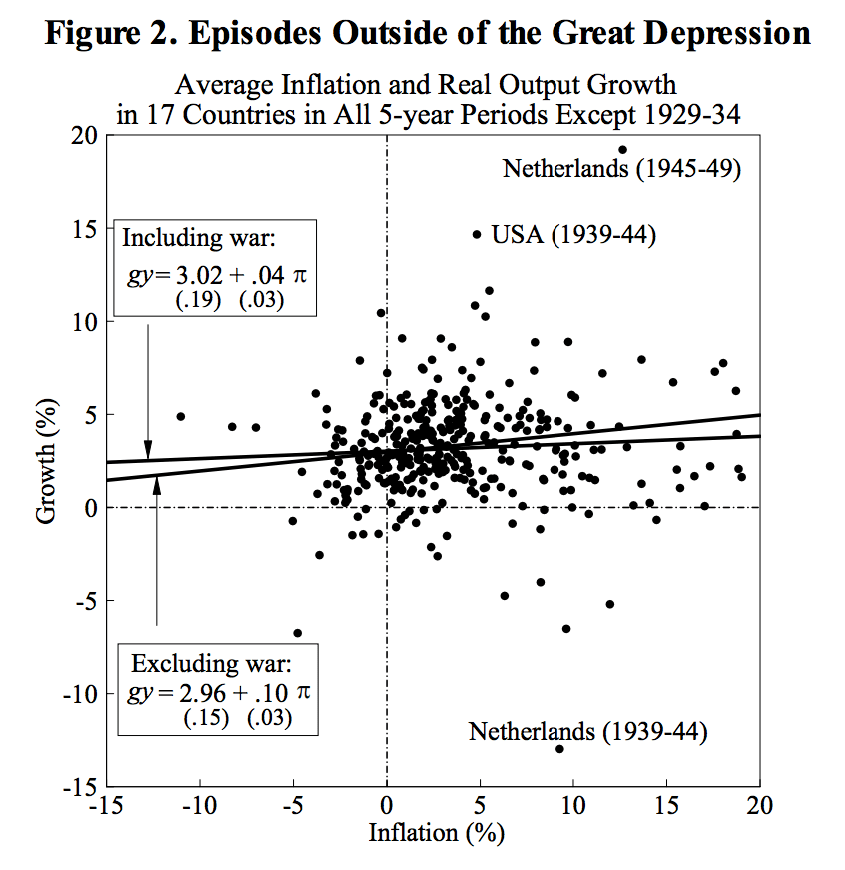

There is a relationship between inflation and output in the following graph.

This is only using data from the Great Depression. Here the relationship between deflation and depression is strongest.

However, outside of the Great Depression (where there are many more data points), there is virtually no relationship between deflation and depression.

The Federal Reserve Bank itself — the Minneapolis branch, created this research. And a natural question arises.

If there is such a weak relationship between deflation and depression (and this includes the impact of confused caused and effect), and if the primary logic for targeting a 2% inflation rate is to prevent depression, then why are so many countries, including the US, continuing to target a 2% inflation rate.

Conclusion

This was an odd article to write. Normally when we write an article, we perform the research that allows us to say definitively what the answer in on a topic. However, in this case, it does not appear than any of the central banks that target a 2% inflation rate know why they do so. They have a “hunch” that keeps an economy in the proper range, but they don’t know why and they don’t know if it is true. This looks like groupthink and is not consistent with the Federal Reserve’s own research (at least one paper, but a seemingly conclusive one) on the topic.

The fact that in the US at least, interest rates on savings accounts (that is non-risk interest rates) are so close to zero, and lead to the loss of value every year for individuals who are not willing to risk their principle undermines the argument by the Federal Reserve or the banking system that there is a genuine concern for the citizens. The fact that the non-risk interest rate on savings around is roughly 2% lower than the inflation rate means that ordinary citizens are providing a subsidy to banks. This adds to the money-making ability of banks that have the power of fractional reserve banking. It would seem that a basic tenant would be that the interest rate on savings accounts would not only match inflation but would also not be taxed (why are capital gains being paid to the government if there are not REAL capital gains being made)?

There is a possibility that the stated reason for keeping inflation at 2% is not the actual reason. This is particularly likely because a.) the central banks cannot provide a solid reason for the 2% target and b.) Evidence contradicts the target being necessary to stopping contractions or depressions. The Federal Reserve or banks rigging the system to have savings account interest rates at close to zero is just one benefit. But there are other reasons to have a constant low level of inflation.

- Reducing Pension Payouts: A constantly low inflation rate also reduces the payouts by companies and the US Government, as most pensions are not indexed to the inflation rate.

- Illusory Salary Increases: It means that when a company gives out a 2% or 3% salary increase, it creates the illusion of progress, when in fact nothing changed. It allows a company to keep the wages the same from year to year, and after three years have passed, most employees will not calculate that they are actually working for less than when they started with the company.

Cost of Living Versus Inflation

There is a second issue, but just as important, which is the cost of living versus the inflation rate. It appears that the cost of living grows faster than the inflation rate. This is a different topic, requiring separate analysis.

References

https://publicpolicy.wharton.upenn.edu/live/news/1068-why-do-we-target-2-inflation/for-students/blog/news.php

https://www.bls.gov/cpi/questions-and-answers.htm

https://www.bankofengland.co.uk/monetary-policy/inflation

https://www.federalreserve.gov/faqs/5D58E72F066A4DBDA80BBA659C55F774.htm

https://en.wikipedia.org/wiki/Inflation_targeting

https://www.economist.com/the-economist-explains/2015/09/13/why-the-fed-targets-2-inflation